The housing market is at a record low for affordability. Not only do we have sky-high prices, but also higher interest rates than usual.

Yes, historically speaking, mortgage rates are in line with the average. We are currently sitting around 6% for a single-family 30-year fixed.

However, housing prices are the highest they have ever been; therefore, mortgage payments are through the roof. Prospective homebuyers need relief.

Dividend Investing in Your 60s

Beware of the snake-oil salesman. Where there is a will, there is a way. A new product will come along when a bunch of people want something but don’t have access to it.

I recently read an article on SeekingAlpha about a new 40-year interest-only mortgage. We don’t have the finer details of the mortgage, but we can speculate.

We can assume that if this product does well, more companies will begin to offer it to customers. Today, I want to examine what this 40-year mortgage can provide you with versus a traditional 30-year fixed payment.

Where do you live? The first question to answer is, where do you live? Do you live in a small, somewhat affordable town or a big, outrageously-priced city?

How to Buy an Expensive Home Safely

I recommend getting the 30-year amortized mortgage (standard) if you live in a somewhat affordable town. You can always add a roommate or house hacking to increase your income.

Buying a home in a big city is much different because the bank wants to see the cash flow to cover the payments. It’s tough to buy a house for $1.5 million when the payments are $8,000/month, and you make $12,000.

The bank wants to see a massive difference between income and expenses (cash flow), which will be hard to overcome.

Enter the 40-year mortgage. How can the 40-year mortgage help? Hopefully, it can get your monthly payment low enough that your bank accepts it.

Don’t Fumble the Bag

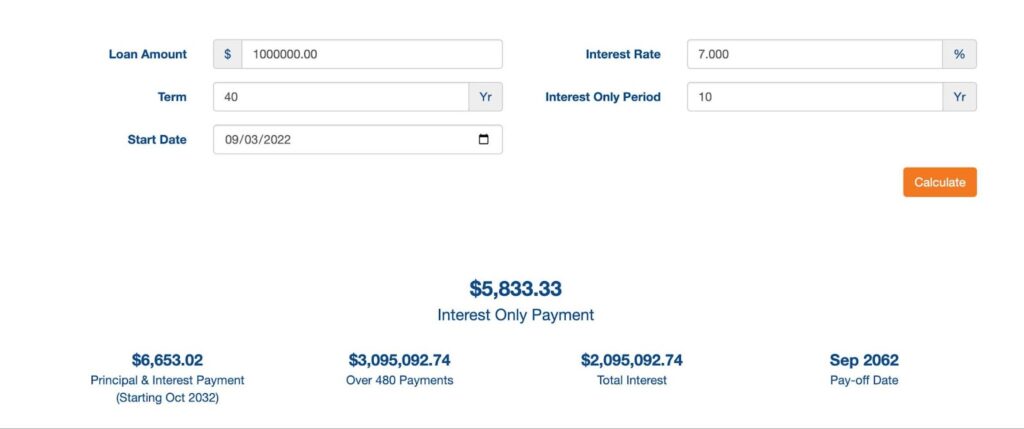

Let’s run the numbers to see the difference. I was able to find a 40-year interest-only calculator on NewFi.

Let’s review the numbers for a $1 million home. I made the interest rate 1% higher because I am sure you won’t get the lowest rate on a 40-year mortgage.

The payment for the 10-year interest-only period is $5,833. Then it jumps to $6,653.02 for the next 30 years. Over 40 years, you will pay a whopping $3 million for the home.

Successful People Need the Most Help

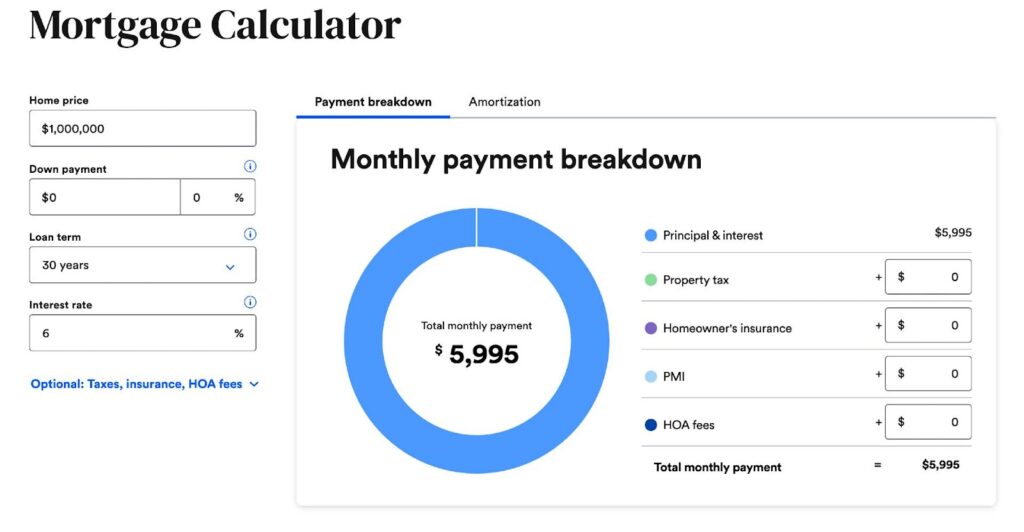

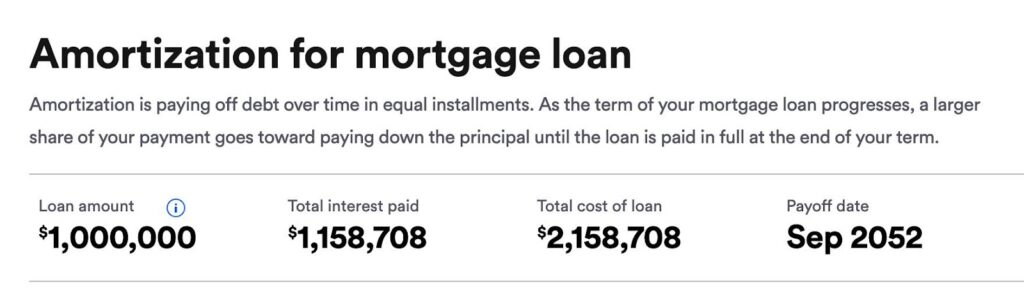

Let’s run the numbers on a standard 30-year amortized mortgage with a 6% interest rate. I did not include taxes and insurance because the loan above doesn’t have them.

The payment is nearly identical, and you pay a total of $2.1 million over 30 years. Numbers never lie.

Key takeaways. I do not see a true benefit of a 40-year interest-only mortgage currently. Again, maybe these new products offer something different.

If they offer lower down payments, that could help families in the long run, but we have to understand interest rates to benefit long-term.

Where are interest rates heading? With inflation still raging through the markets, the Federal Reserve is promising to keep interest rates higher than in the last 15 years.

Passive Income Road Trip #7: Automated Business

Since 2008, we have become used to living in a low-interest-rate environment. Now, it’s time to move into a period where the Federal Funds rate will stay between 4-6%.

This means that the 10-year Treasury will stay between 5-7%, and mortgages will stay around 6-8%. This may be the new normal for the next ten years. We need to adjust to this new world order.

I am looking forward to buying 30-year Treasury Bonds at higher rates. It will be my monthly investment, along with my dividend stocks.

Where are housing prices heading? Yields and prices have an inverse relationship. When interest rates rise, prices should fall. However, this may not be the case.

The Emotional Roller Coaster of Debt

A couple of factors will keep housing prices higher than average. First, there are still cash buyers. Cash buyers can come from a lot of different sources.

Cash buyers can be US investors, foreign investors, real estate investment trusts, and institutional buyers (pension funds).

They can also be regular Americans cashing out of their homes in California and New York and moving to Alabama and Florida. As prices begin to fall, people will inevitably start to sell to take profits.

The second item that will keep prices higher is the great mortgage reset. The common wisdom was to pay less than 33% of your salary to housing. Over the years, and with both parents working, this has jumped to 50%.

Now, it’s more typical to be house-rich and cash-poor, and people are willing to pay the price. So, as soon as there is a deal, expect someone to come along to purchase it.

Start a Sports League towards Passive Income

If we all went on a home-buying strike, we could lower prices rather quickly, but that is not the case.

How to afford a home. You will have to sacrifice something to get into a home over the next ten years. With mortgage rates between 6-8%, housing prices would need to come down 20% to be affordable.

I don’t see the market dropping that much, maybe 5-10%. You have to create new sources of income, such as an online business or room rental, to save for a down payment.

You can earn a considerable salary while working remotely in a small Georgia, Alabama, and Florida city. Don’t forget you can get cheap land in some places.

The Magic of a Sales Funnel

You can buy land and drop a mobile home or tiny home relatively inexpensively. My wife and I were checking out mobile homes for $110,000, which were lovely. We have three acres of land and can add multiple homes to the property.

Conclusion. Don’t let the shiny veneer of a 40-year interest-only loan trick you. It’s snake oil at the moment.

If interest rates were heading downwards, they might have been helpful. You could use the loan and hope to refinance in five years, but that is not the case.

Income Investing vs. Index Funds

To get into a home, you must do the work—log more hours at your job, find a remote work position, become a content creator, invest for dividends, or start a business.

There is no easy answer or one-stop-shop solution to the current housing crisis. Finding a deal in your neck of the woods will be tough. So you can either move somewhere else or bring in more money. Those are your two options. Good Luck!

- PDF of the Month: Retire Rich with a Business 4 (Free 149-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 2 (165-Page Free PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 2 (Free 123-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 2 (Free 185-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 7 (Free 424-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 2! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out on Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Crypto Exchange: My Favorite Crypto Exchange VOYAGER (Join Voyager)

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: REITs vs. Homeownership (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply