My Dividend Debit Card has been popping off recently. I am getting close to $200/month on my Cash App Debit card—which I refer to as my Dividend Debit Card.

More importantly, my wife has a Dividend Debit Card, and she loves getting her fresh cash flow monthly. It’s a great system and puts your money at your fingertips.

Today, I want to review how we arrived at this point in our investing journey and look toward our cards’ future. Let’s begin.

How We Plan to Retire on Dividends 3

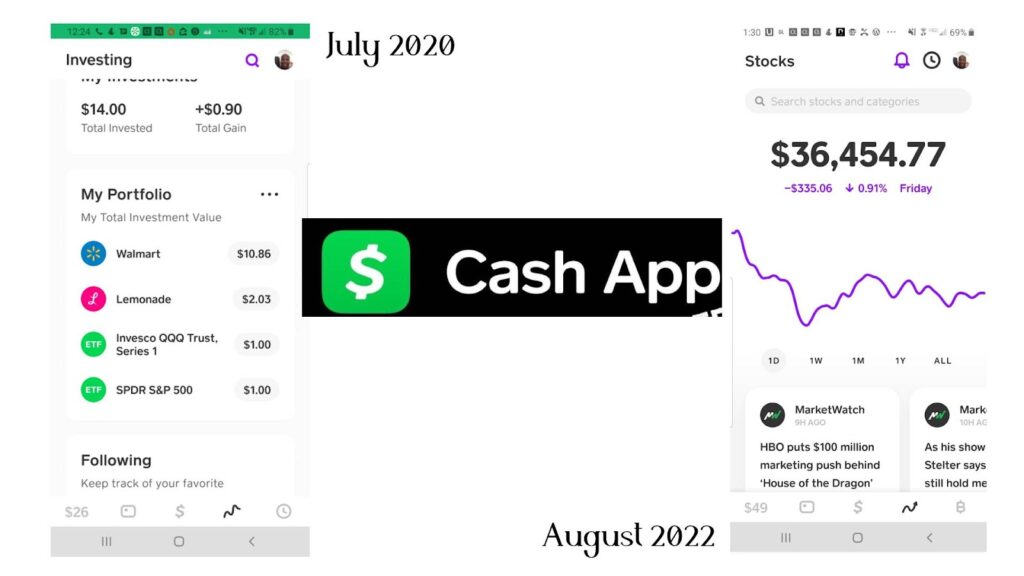

Starting my Cash App. Like everyone else, I initially used my Cash App solely for money transfers. However, I learned that the app allowed stock market investing in July 2020.

In that same month, I invested $69 in stocks. I found an old blog post regarding my Cash App from July 10, 2020. It’s incredible to see where we started.

Today, I have over $36,000 in my Cash App and heading towards $100,000. More important is the cash it spits off every month. Let’s talk about cash flow.

What is cash flow? Cash flow is the income from your investments. You can consider the money from your job as cash flow, with your investment being time.

However, we want our money to work hard for us, so we invest for dividends. Waking up to an email or notification saying you have new cash never gets old.

Happy Cash Flow Retirement 7

The fundamental goal of the Dividend Debit Card (DDC) is to get your cash flow directly where you need it most, in your wallet.

The Dividend Debit Card vs. Inflation. In 2022, inflation has wreaked havoc on the economy and our budgets. I wrote an entire series to help people better navigate these inflationary times.

- Inflation Ate My Paycheck 101: Adjust Your Lifestyle Today

- Inflation Ate My Paycheck 102: 10 Creative Ways to Beat Inflation

- Inflation Ate My Paycheck 103: Creative, Investor, Tycoon, Entrepreneur

- Inflation Ate My Paycheck 104: Create Infinite Dividends

- Inflation Ate My Paycheck 105: From Broke to Saver to Investor

- Inflation Ate My Paycheck 106: Time to Start Couponing.. Or Not

- Inflation Ate My Paycheck 107: Cellphone Upgrade vs. Dividends

The DDC helps us overcome inflation by giving us that extra spending power we need during these times.

My wife likes to save her dividends until something random pops into her life. It could be a course she wants to take or something for the kids.

Retirement Plus: Use Royalties to Supplement Your Retirement

I also like to have my dividends pile up in my account. However, my random spending usually involves blue-chip stocks going on sale.

Getting started with your DDC. So, how do you get started with your own Dividend Debit Card? Cash App is a great application to start your dividend investing portfolio.

Also, I am experimenting with a DDC with M1 Finance. The basics will be different, but more on that one later.

First, create your Cash App account. Then at the bottom, you’ll see a place to invest in stocks and Bitcoin. You can read the article “Your First Five Dividend Stocks,” which will guide you along the way.

Build Your Rep: Create Your Body of Work

Keep investing. But you can’t just put in $500 and think it will pay you tons of dividend income. Unfortunately, dividends require lots of money to make a difference in your life.

Every paycheck, I invest roughly $400 into my DDC, and my wife puts $500 into hers. We plan to keep investing until the end. It is fun to watch your dividend income grow over the years.

But you have to start somewhere. Don’t forget to celebrate your wins along the way. For example, you may want to eat out for $20 with dividends or spend $45 on nails.

Take small steps with your dividends, and you will slowly build up your spending power. Remember, “what gets rewarded gets repeated.”

The DDC in our overall passive income plans. We want our DDCs to be our completely guilt-free money account. I have five brokerage accounts, and my wife has four.

Retire By Age 38 in this 10 Difficult Steps

We use M1 Finance as our income portfolios, Stash as our Dividend Growth, and Wells Fargo as a little of both.

Our DDC will allow us to spend freely, especially as we move overseas. Hopefully, we will arrive at $1,000/month from our Dividend Debit Cards.

We can keep all the other accounts growing in the background, as our DDC functions as our expense (fun) money. It’s a great life and one I hope you consider.

Cash App limitations. Cash App does have some restrictions. Your dividends will arrive a couple of days later than their official payment date.

Can You Retire on Dividends from Index Funds

That is because each dividend has a clearing time. It is the same in brokerage accounts; however, they will let you reinvest them without the clearing time.

Also, the Cash App doesn’t have the best selection of income-investing products I love. They don’t have closed-end funds, preferred shares, and dividend ETFs.

As much as I love my income products, it is good because I have to research high-yielding blue-chip stocks like Gilead (GILD) and Omega Health Investors (OHI).

Fundrise vs. USDC

Conclusion. As I wrote in “How to FALL into Investing 2,” now is the season to get into dividend investing. Why use your job as your only source of income?

We are moving into a new phase of the recession, and nobody knows what the real estate, stock, and crypto markets will bring.

Prepare yourself by building an additional income while taking advantage of mispriced income stocks. Trust me; even an extra $200/month in dividends is life-changing.

Do you want to spend your entire life waiting for a pay raise from your employer or the government (social security)? If not, you’ll have to learn how to invest—the time is now. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 7 (Free 424-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 2 (165-Page Free PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 2 (Free 123-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 2 (Free 185-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 6 (Free 409-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 2! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out on Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Crypto Exchange: My Favorite Crypto Exchange VOYAGER (Join Voyager)

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: REITs vs. Homeownership (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply