Investing is about getting a return on your investment, therefore ensuring the velocity of money, compounding, time, and intellect all work in your favor. The more you learn, study, and grow, the better your chances are to get “lucky.”

When we think about investing, sometimes we come to decision points that lead to vastly different outcomes. Today, I want to discuss the difference between two 9% yielding strategies: income investing and USDC stable coin.

These strategies require entirely different education, serve different purposes, and require different levels of risk. However, does achieving 9% with each approach lead to the same outcomes? Let’s have a look.

Happy Cash Flow Retirement 2

What is Income Investing? Income investing is investing in the stock market with the sole purpose of achieving a high level of income. The majority of people who invest in the stock market do so for growth.

With income investing, you sacrifice growth (capital gains) and instead take your profits in the form of a high dividend yield. We invest in securities such as business development companies (BDCs), mortgage REITs, bond funds, closed-end funds, high yield blue-chip stocks, and preferred shares to achieve high yields.

What is USDC? Investing in cryptocurrencies can be intimidating to the average person. However, it doesn’t need to scare anyone. USDC is a stable coin that corresponds to the US Dollar. USDC mints a coin every time someone uses a US Dollar to purchase a USDC coin.

This connection ensures that USDC and the dollar stay correlated. USDC is basically a digital dollar that you can use in centralized and decentralized finance.

My favorite centralized platform, Voyager (affiliate link), pays 9% (annual) interest on USDC, which hits your account every month. The price of USDC does not fluctuate; it stays fixed at one US Dollar.

How to Start Dividend Investing 104: Choosing Your Stocks

Shopping at a discount. The significant difference between an income portfolio and USDC is the ability to buy at a discount. Purchasing high-yield products on the stock market have an advantage and disadvantage over USDC—the products trade on the emotions of the stock market.

Because the stock market can become irrational at times, you’ll be able to find great deals on high-yield products. If you understand the market and follow it daily, you can walk away with yields much greater than 9%.

Over time, you can accumulate very high yields by investing in discounted securities. Let’s look at some of the deals on various high-yield products.

- High Yield Blue Chip stocks. High-yield stocks like AT&T (T), Altria (MO), and Phillip Morris (PM) are always in the news. When fresh tobacco news hits the media, Altria may drop in price between 5-10%. Buying on days like this can significantly increase your yield.

- Mortgage REITs. Mortgage REITs like AGNC (AGNC) and Annaly Capital (NLY) have extreme highs and lows based on future interest rate changes. It’s not uncommon to see yields between 10-13% on bad days in the market. I buy on these opportunities because I understand the business aspects of mortgage REITs.

- Closed-End Funds. CEFs use leverage; thus, raising interest rates can lower their appeal on the stock market. If you buy high-quality CEFs, like those from PIMCO, these dips are great buying opportunities.

M1 Finance for the Win. If you want someone else to do the heavy lifting, M1 Finance can assist you. You can create an income pie with your top income choices.

The Business of Being Busy

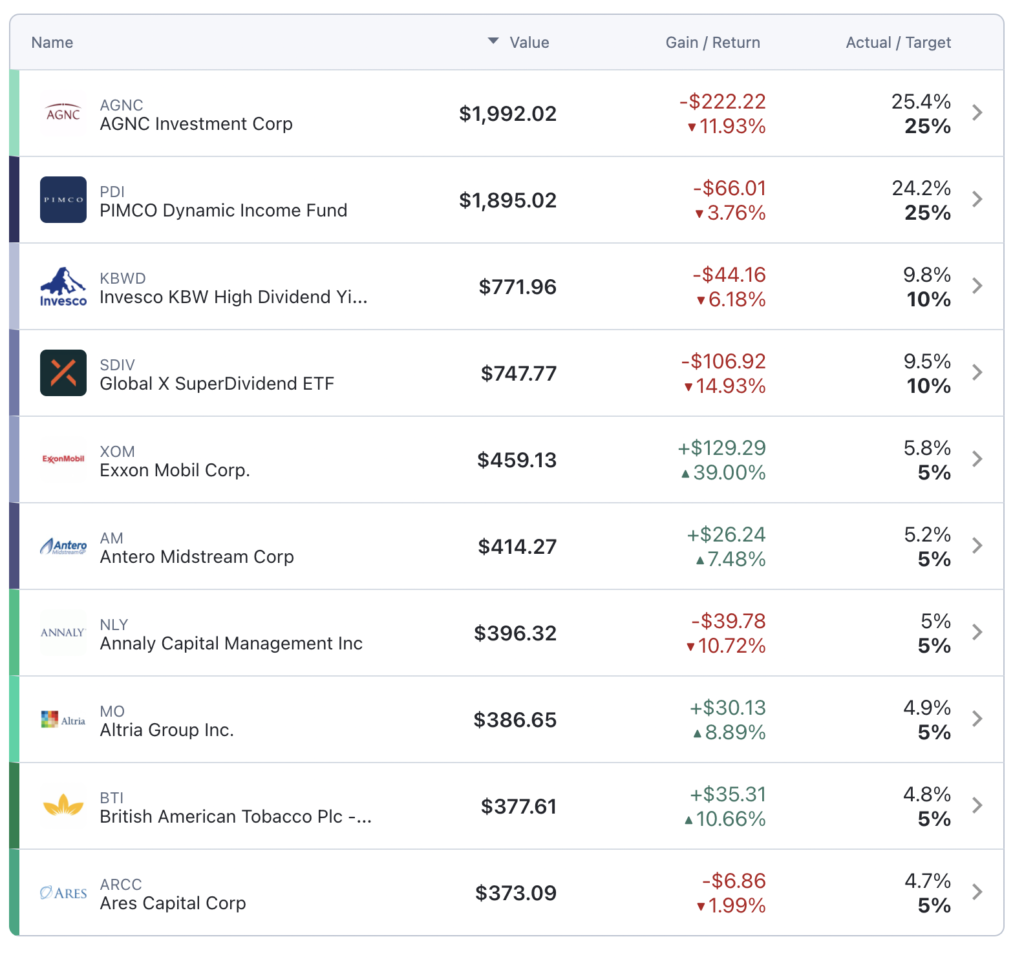

You can dollar-cost average into the pie, and M1 Finance will find the best deals the day you are buying. Over time, your yields will exceed 9%. Here is a look at my income portfolio of M1 Finance.

Due to the threat of war, inflation, interest rates, and more, these securities struggle in the market. Again, these are buying opportunities if you believe in the long-term health of the United States.

Why is USDC important? If my income portfolio can easily generate 9%+, why would I need to purchase USDC? USDC trades entirely outside the stock market, making it vital to our overall plan.

Blogging to Financial Independence

Currently, the FED is attempting to raise interest rates, lowering prices on high-yield products. However, when rates are at 0%, people seek high-yield products. This means that prices go up and dividend yields go down.

So, during a bull market, I may only be able to achieve a 7-8% yield on a good day. People flock to yield during bull markets, leaving income investors stranded.

This is an excellent time to buy our consistent USDC. Instead of trying to buy closed-end funds, BDCs, mortgage REITs, etc., at all-time highs, we can get a great yield on USDC. It makes for a great yin & yang situation.

Long-term prospects. You can achieve high yields and capital appreciation with income products if you buy great opportunities. Remember, we are buying when prices are low and achieving high yields.

Real Estate is a Mindset (Beginner)

When the market recovers, we also achieve high capital appreciation. Imagine how much income your portfolio can produce if you continually do this for 10-20 years.

However, there is something about having your money in a specific product like USDC. This is especially important if you are retiring to a homestead or overseas.

If something happened today, I would not want to liquidate my income portfolio because my prices are down. I would leave my income portfolio alone.

However, this would be a great time to utilize my USDC portfolio. I could easily withdraw whatever I needed for my emergency and put it back over time.

So having $200,000 in USDC and $200,000 in an income portfolio would serve two completely different purposes. I can use USDC for income and as an emergency fund. I can use an income portfolio for income, growth, and generational wealth.

What Limiting Beliefs Do You Have About Money?

Conclusion. As we prepare for an unknown future, we know at least one thing—we will need income. Both USDC and an income portfolio will give us a large revenue pot.

However, their use-cases over time will diverge and serve different purposes in our overall portfolio. USDC will serve as an income generator and emergency fund, while an income portfolio will serve as a paycheck replacement and generational wealth for our children.

So the winner is BOTH. These strategies differ enough that investing in both over the long term will set you up for a higher success rate than using only one.

These principles work best together in a yin & yang style investing technique. Ensure you do the requisite due diligence on all securities you buy, and you can achieve excellent yields with low risk.

- PDF of the Month: Don’t Gamble with Retirement 6 (Free 409-Page PDF)

- Free PDF Downloads: Download FREE PDF books here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 2 (165-Page Free PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 2 (Free 123-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 2 (Free 185-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 5 (Free 431-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 2! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Crypto Exchange: My Favorite Crypto Exchange VOYAGER (Join Voyager)

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 54 Takeaways from 54 Books (book)

- Writing: Can Grammarly Make You a Better Writer?

- My Favorite Chromebook: The Ultimate Chromebook (direct)

- Follow us: On our Facebook Page and Join our Facebook Group

- Monthly Dividend Tracker (XLSX): Check it out on Etsy

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply