There are more ways to save and invest than ever, yet most Americans have less than $1,000 in savings. Dave Ramsey (“Baby Step Millionaires”) suggests saving a $1,000 emergency fund before paying down debt.

I have been talking about saving and investing recently, and even savings vs. investing. But, just because you are not comfortable investing doesn’t mean you can’t get an excellent return on your savings.

The original savings accounts. Long are the days where you must keep your money in a savings account earning 0.01% per year. If you saved $100,000 in a standard savings account, you would make $10 per year. That’s just insane.

The Passive Income Hero 2

High Yield Saving Accounts. Nowadays, many banks provide online services only, which reduces overhead costs. They can pass these savings onto consumers. My favorite high-yield savings account is from Discover bank.

Discover currently pays 0.4% interest, which isn’t much. However, it is 40 times as much as a standard bank. I will write an entire article on my three years of experience with Discover.

The comparison. Today, I want to talk about three other options to get a return on your savings. I consider these safe places to park money—with USDC stable coin being the riskiest.

I will compare Savings “I” Bonds, Treasuries (30-year Bonds), and USDC to see which is the best place to park your money for the long run. Also, I will run a scenario on how I would invest $200,000 total across these three accounts. Let’s proceed with our comparison.

Saving “I” Bonds. Let’s start with Saving “I” Bonds. You buy them from the US government at the TreasuryDirect website. These bonds are unique because they offer inflation protection.

With inflation currently sky-high, “I” Bonds are yielding 7.1%. This may not always be the case, but I look forward to high yields for a couple of years.

The Balanced Writer

“I” bonds reinvest their interest payments back into themselves, so you don’t get interest payments until you sell them or they reach maturity. This means you don’t buy them for current income payments.

30-Year Treasury Bonds. There are four types of Treasuries, but my favorite is the 30-Year Bond. 30-Year bonds pay semi-annually so that you can invest for current income.

The 30-Year Bond is currently paying 2.25%, which isn’t horrible. However, this is not ideal, with inflation hitting over 7% last month.

To invest successfully in 30-Year bonds, you must understand inflation risks, safety of principal, and interest rates.

When NOT to Use Credit Cards

I may not be a 30-year bond investor today, but I am also only 41 years old. If I was 80 years old, with $200,000 to invest, the income from a 30-Year Bond might be acceptable.

The interest on $200,000 (at 2.25%) would be $4,500/year or $375/monthly. Not too terrible; maybe you could use that as a vacation fund or dining out allowance.

USDC Stable Coin. USDC is my favorite saving product on the market; however, I can see many people afraid to invest in cryptocurrencies.

To invest in crypto, you must understand the larger financial landscape. We are moving into an age where we depend on digital transactions (the metaverse) more than ever. Stable coins like USDC will act as digital cash versus other cryptos that serve as investments, stores of wealth, and smart chain currency.

If you are on the fence about investing in centralized markets, I highly recommend reading both “How to DeFi -Beginner” and “How to DeFi -Advanced.”

USDC acts like a digital US dollar but interacts in the crypto space. Voyager (affiliate link) pays 9% interest for you to hold your USDC with them. Yes, 9%!

The Magic of Being a Content Creator

If I had $200,000 in my USDC account on Voyager, I would receive $18,000/year or $1,500/month. That is an excellent wage and can really turbocharge your savings.

Which is the best? While I prefer USDC, I also have many other investments. I have a military pension, dividends, royalties, rents, and USDC. So, I am not 100% dependent on my stable coins for income.

You may be in a different boat. It all comes down to how much income you need and your risk tolerance. No one can tell you what investments will allow you to sleep at night.

However, using all of these investments together will allow you to achieve the best results. They all have their place in your portfolio; you’ll just have to decide which allocation suits your needs.

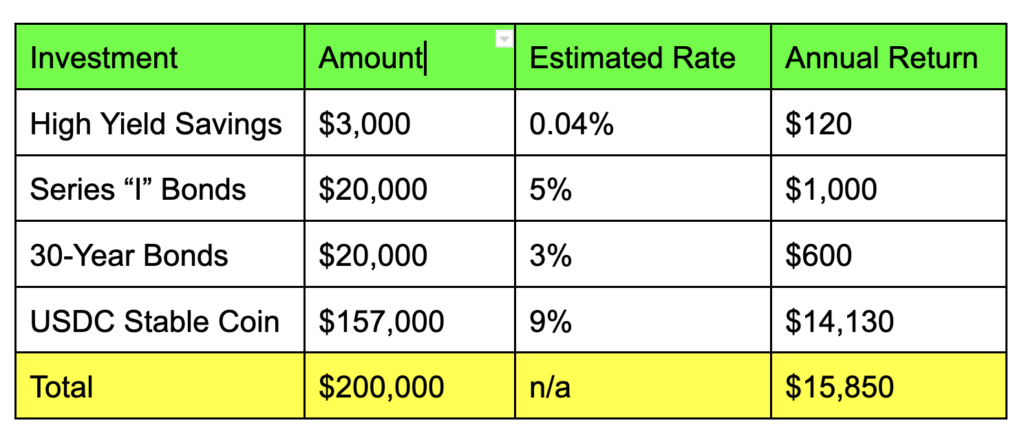

How I would invest $200,000. If I had $200,000 to invest into these products, this is how I would allocate my funds.

As you can see, I skew my allocation heavily towards USDC. Over time, I may decide to reduce my stake in USDC and move into bonds more.

How to Create Passive Income 104: For the Average Person

I could also decide to keep more money on hand in my high-yield savings accounts. The more options I have, the better choices I can make.

Conclusion. Being a saver doesn’t mean you cannot earn a return on your savings. The stock market doesn’t affect any of these investments.

You can invest in these products and forgo the highs and lows of the stock market. However, using these plus the stock market can allow you to F.I.R.E. in style.

Which of these savings investments is your favorite? Do you need to research more into the other types? Join my Facebook Group to discuss further. See you there!

- PDF of the Month: Counting on Crypto 2 (Free 159-Page PDF)

- Free PDF Downloads: Download FREE PDF books here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 2 (165-Page Free PDF)

- Cryptocurrencies: The Magic of Cryptocurrencies (Free PDF)

- Real Estate: Financial Independence through Real Estate 2 (Free 123-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 2 (Free 185-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 5 (Free 431-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Crypto Exchange: My Favorite Crypto Exchange VOYAGER (Join Voyager)

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 54 Takeaways from 54 Books (book)

- Writing: Can Grammarly Make You a Better Writer?

- My Favorite Chromebook: The Ultimate Chromebook (direct)

- Follow us: On our Facebook Page and Join our Facebook Group

- Monthly Dividend Planner: Check it out on Etsy

- For more detailed analysis, join my Youtube: MFI YouTube Channel

New Year’s Passive Income Resolution 2022: Article (Amazon Book)

New Year’s Passive Income Resolution 2022: Blank-Lined Notebook (Amazon)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply