How do I get started with investing? Why do I need to invest? How much money do I need to invest? What do I need to invest in with my money?

These are some of the questions that are keeping you from investing. And since you know that you need to invest, these questions are actually limiting beliefs.

Styles of investing. There are many styles (types) of investing. You have index fund investing that allows you to invest large amounts of money into simple funds that (almost) can’t fail.

Dividends vs. Capital Gains 2

Then there is dividend growth investing. DGI is the process of investing in proven, blue-chip dividend-paying stocks. Over time, the power of compounding will give you a massive stream of income.

Finally, there is income investing. Income investing seeks immediate income using closed-end funds, business development companies, real estate investment trusts, etc.

Dollar-cost averaging. No matter your investing style, using dollar-cost averaging (DCA) is the best way to maximize returns, avoid buying at the top, and feel less pressure about investing.

What is DCA? DCA is the art of investing consistent amounts of money at consistent amounts of time. Consider it your investing schedule.

Today’s powerful apps and websites can help you plot your investing calendar faster than ever before. There is truly no reason why everyone can’t invest.

Art Edition: The Biggest Book on Passive Income Ever!

You can invest daily, weekly, or monthly. You can invest in individual stocks, index funds, ETFs, or entire investment pies.

The Magic of DCA. The magic of DCA is that you buy more shares when the price is low and fewer shares when the price is high. Over time, this strategy leaves you in positive territory.

Let’s look at how you can utilize DCA to grow your investment portfolio.

- Consistent amount, random stocks. I use this strategy with my Cash App account. I receive my paycheck and immediately invest $500 into the Cash App. However, the stocks vary each time I invest. This is good and bad. Good because I can diversify and can find good deals. Bad because it takes more time, and you can feel more fearful when looking at prices.

- Daily. I do not use it daily yet, but I would use it with M1 Finance pies if I did.

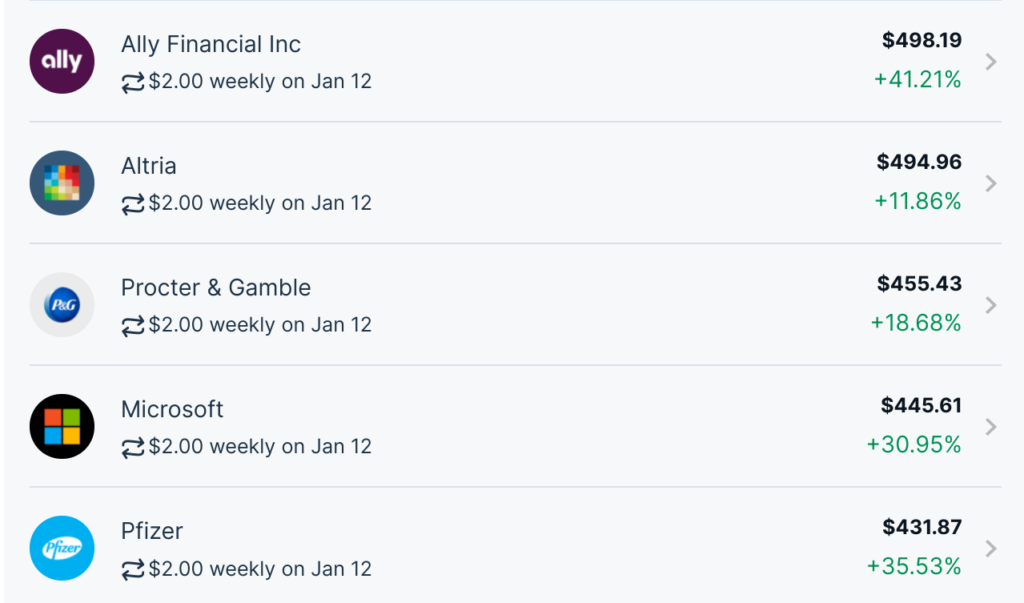

- Weekly. I use weekly DCA with my STASH portfolio. Every week, I invest $2-5 into over 20 different positions. This has provided me with over a 20% gain to my overall portfolio. My STASH account is what I consider a dividend growth portfolio.

- Monthly. I like to use monthly DCA investing with my M1 Finance pies. This way, when I invest $600 into my M1 Finance pie, it gets evenly distributed across my many different positions. This allows M1 Finance to find the best deals and buy the lowest-priced securities.

- Dividends. I allow my dividends to accumulate as free cash inside my Wells Fargo account. I then can spend my money back into the portfolio, buying the best deals.

- Automatic Dividend Reinvestment. My STASH and Charles Schwab accounts automatically reinvest dividends directly back into the stocks that paid them. This provides monthly or quarterly DCA, depending on the stocks.

Reduce fear. When I first started dividend investing (June 2019), I was terrified of buying stocks at all-time highs. I remember contemplating buying McDonald’s at $210, worried that this was the top.

Today, McDonald’s sits at $267. That’s why it is so much better to DCA into these blue-chip stocks. Every week, I use STASH to invest $2 into 20 blue-chip stocks like McDonald’s (MCD), Altria (MO), T. Rowe Price (TROW), and Procter & Gamble (PG).

52 Weeks of the Dividend Challenge

The best part is you don’t have to look at the stock price each week. I just drop my $2 into the pot and see what happens.

Automatic investing. M1 Finance handles dividends a little differently. Once your M1 Finance pie reaches $25 of dividends, it then sprinkles this cash across the pie, starting with the best-priced stocks.

My next M1 Finance income portfolio goal is to get my dividends up to $100/month. Then that $100 will DCA across the income pie. This means that the pie would automatically spend $100 to buy what’s on sale. This method will make you rich by automatically buying the highest-yielding securities.

Getting started with DCA. I recommend STASH as the first place to create a brokerage account. You can start by setting up a $5 weekly DCA into my favorite index fund, VTI, the total stock market. It is difficult to go wrong with the entire stock market.

Once you get the hang of DCA, you can add other blue-chip stocks, bonds, REITs, or dividend ETFs. The world is your oyster at this point.

The most important part is to take your time. There is no rush to get rich here. Just by opening up a brokerage account, you are way ahead of the general population.

Remember to stay motivated during your passive income journey. Set small goals like “receive $10 a month” in dividends. Once you reach these goals, always celebrate your victories—what gets rewarded gets repeated.

Let Dividends Be Your Lighthouse through Retirement

Conclusion. Dollar-cost averaging is the technique most of us should use to become rich. If we want to get richer faster, we insert more money into the program.

If we try to put a lump sum of money into a “high growth stock,” or cryptocurrencies, we risk our capital by speculating. We don’t want to do this.

We want to DCA into proven index funds and blue-chip dividend stocks. Yes, it won’t be sexy to watch your McDonald’s stock give you 20-30% returns over 3-5 years, but you are growing your wealth and income potential. All while doing it safely.

I love looking at my year-over-year returns. That is the best metric to gauge your investing success. In December 2019, we had $64 in total passive income. In December 2020, we had $133 in total passive income. And in December 2021, we had $1,083 in total passive income.

These techniques work if you stay consistent and continually motivate yourself to keep on the path. You can also join my Facebook Group, and we can encourage each other. Good luck!

- PDF of the Month: Become CEO of Yourself 2 (Free 196-Page PDF)

- Free PDF Downloads: Download FREE PDF books here

- Financial Mindset: Become CEO of Yourself (book)

- Retirement Planning: Don’t Gamble with Retirement 5 (Free 431-Page PDF)

- Investing: How We Plan to Retire on Dividends 2 (165-Page Free PDF)

- Cryptocurrencies: The Magic of Cryptocurrencies (Free PDF)

- Real Estate: Financial Independence through Real Estate 2 (Free 123-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 2 (Free 185-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Crypto Exchange: My Favorite Crypto Exchange VOYAGER (Join Voyager)

- Kindle Unlimited: I Why Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 54 Takeaways from 54 Books (book)

- Want to Build Passive Income from Books and Affiliate Marketing? (Learn here)

- Writing: Can Grammarly Make You a Better Writer? (direct)

- My Favorite Chromebook: The Ultimate Chromebook (direct)

- Follow us: On our Facebook Page and Join our Facebook Group

- Amazon Author Page: Check out my author page on Amazon

- Monthly Dividend Planner: Check it out on Etsy

New Year’s Passive Income Resolution 2022: Article (Amazon Book)

New Year’s Passive Income Resolution 2022: Blank-Lined Notebook (Amazon)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply