There has never been a better time to make the switch from a capital gains investor to a dividend investor. In fact, I would classify most capital gains-lovers as traders. As we move into an inflationary period, the growth stocks that many capital gains traders love may not outperform as they did over the last five years.

I wrote the original “Dividends vs. Capital Gains” over a year ago, and things were much different on the stock market. Amazon, Apple, and cloud service stocks were outperforming the stock market by a large margin.

The index fund that tracks the Nasdaq (QQQ), considered to follow growth stocks, destroyed the Dow Jones Industrial Average index (DIA), which tracks value stocks. However, in early 2021, we started to see a rotation from growth stocks to value stocks. Why?

Why Is Talking About Money Bad?

Why are people rotating from growth stocks to value stocks? Growth stocks (capital gains) usually don’t pay dividends. Some may pay dividends but are very small (less than 1%), as is the case for Apple (APPL) and Microsoft (MFST).

When a growth stock has earnings, they reinvest the earnings back into the company. So investors don’t see the profits via dividends, but they see the share price rising. However, the investors base the share price on multiples of future earnings. This is called the price to earnings ratio or P/E.

Currently, Amazon (AMZN) has a P/E ratio of 64. This means that the stock market is pricing in a large amount of growth in Amazon’s future. However, inflation drags down future earnings because money today is worth more than money tomorrow.

Indeed, growth stocks that have outperformed in the past may be slowing down. On the flip side, dividend stocks are much easier to evaluate. Their P/E ratios are much lower, which is why they get the term “value stocks.”

Choosing dividends stocks. Phillip Morris (PM), one of my favorite dividend-paying blue-chip stocks, has a P/E ratio of 16. The dividend yield of 5.28% means that you can at least keep up with inflation or beat it slightly.

Stocks vs. Bonds: Is 60/40 Still Effective?

Understanding why dividends are a great way to beat inflation is vital to becoming a bonafide investor. I know that I did a deep dive on P/E ratios, but it is essential to speak the language of the stock market.

Inflation is upon us, and looking to capital gains to beat inflation may not be the best strategy. Let’s look at the two dividend strategies that I employ to beat inflation, dividend growth investing and income investing.

Dividend Growth Investing. I use the mantra “Build Wealth Slowly” for all my investing decisions. Dividend growth investing is the definition of slow, comfortable growth. The idea of DGI is to dollar cost average into blue chips stocks. Your portfolio starts to compound because you continually buy more shares, the price share prices rise, and the dividend payout increases.

Fundrise vs. REIT Stocks

Over time, your portfolio increases, and the amount of income slowly increases as well. When you stop reinvesting dividends during retirement, this leaves you with a considerable source of stable income and growing share prices—not a bad way to get rich.

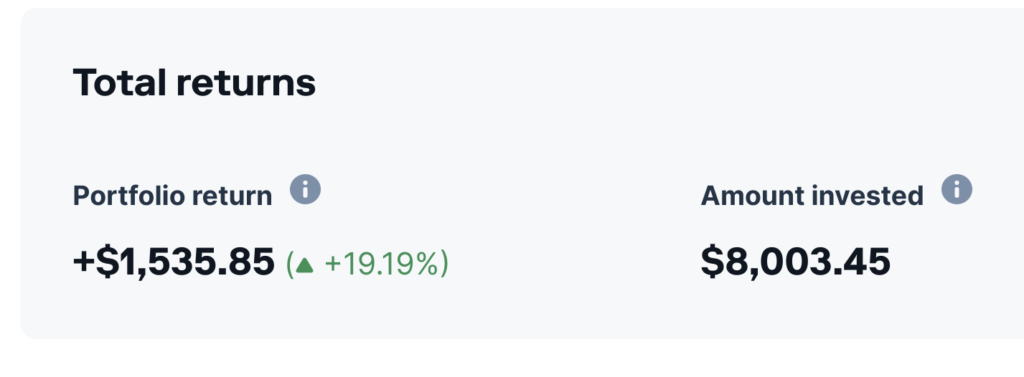

I consider my STASH app to be my pure DGI portfolio. As you can see, because of dollar-cost averaging, I am up 19%. More importantly, I receive $45/month in dividend income from the portfolio, and I have growing positions in 20 stocks.

A capital gains investor might scoff at a 19% gain over two years, but I am more than happy with it. Imagine you put $8,000 in the bank, and not only did it grow into $9,500 in two years, but it paid you over $400. It’s all a mindset that you must conquer to build wealth.

Income investing. Income investing is all about buying high-yield products over time. We don’t expect the share prices to rise much over time; however, we demand they pay their profits via high dividends.

Living Overseas Passively 104: Dividend Income

I just started a new income investing portfolio in M1 Finance, and it is not ready for prime time. However, it currently has a dividend yield of over 8%. Instead of dollar-cost averaging, you allow the income portfolio to buy shares of itself over time.

It will buy high-yield income products when they are on discounts. Over time, you will have a vast portfolio with an excellent yield-on-cost. I have been doing for my SDIV position at Wells Fargo.

I am up 12% over time, but it pays me $146 a year in dividends. Those dividends go back into the position each month. In 10-20 years, I will turn off the dividend reinvestment, and then I have a substantial monthly dividend income to pay expenses. That’s the magic of income investing.

Selling Covered Calls for Passive Income

Capital gains are much more limiting. When you invest in capital gains, you are much more limited in your abilities to allocate capital. Your only option is to sell your shares and take profits. You are also at the whim of the stock market. You can see all your gains wiped out over a day or week because of a scandal.

There is room in your portfolio for speculation, but call it that. I am up 400% on my Cloudflare position. It is a growth stock that I will let grow until the end. But, my overall main objective is to build a retirement income using dividends—not a portfolio of growth stocks.

Don’t Gamble with Retirement 4

Conclusion. Capital gains can be fleeting and unpredictable. Yes, you will always hear your pals at work talking about how much money they made over capital gains and good for them. They won’t talk about how much money they lost, though.

As they talk, I mention that I made $550 in dividends and $700 total in passive income in a month, and they become quiet. Their capital gains don’t pay them anything. I have cold hard cash sitting in my accounts, ready for me to redeploy or spend at my leisure. It’s not a bad life, and I am just getting started.

Please join my Facebook Group if you want the latest articles and free books delivered to your news feed. Also, you can contact me inside the group and ask questions. I also have a Facebook Page where you can see my latest articles.

- PDF of the Month: How We Plan to Retire on Dividends 2 (165-Page Free PDF)

- Free PDF Downloads: Download FREE PDF books here (Twitter Link)

- Financial Mindset: Become CEO of Yourself (book)

- Retirement Planning: Don’t Gamble with Retirement 3+4 (696-Page Free PDF)

- Investing: The Pros and Cons of Dividend ETFs (Free PDF)

- Cryptocurrencies: The Magic of Cryptocurrencies (Free PDF)

- Real Estate: Real Estate is a Mindset (Intermediate) (Free PDF)

- Business: Retire Rich, Retire Comfortable with a Business 2 (Free PDF)

- Everything!: The Biggest Book on Passive Income Ever! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Sign up to Access our “Hidden” Free Kindle Book Schedule

- My first Children’s book: A Child’s First Book on Passive Income (book)

- Book Reviews: 54 Takeaways from 54 Books (book)

- Want to Build Passive Income from Books and Affiliate Marketing? (Learn here)

- Writing: Can Grammarly Make You a Better Writer? (direct)

- My Favorite Chromebook: The Ultimate Chromebook (direct)

- Follow us: On our Facebook Page and Join our Facebook Group

- Amazon Author Page: Check out my author page on Amazon

- Monthly Dividend Planner: Check it out on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply