We have come a long way in our quest to live overseas on passive income. Throughout the Living Overseas Passively series (101, 102, 103), we have explored the mindset we need to acquire and what retirement income we can best leverage to make our lives comfortable overseas.

Now, it is time to present the granddaddy of passive income—Dividends! Dividends are the most passive of all the passive income streams. However, it will take an enormous amount of money to build a healthy stream of cash flow.

Luckily, I have already done much of the legwork for retiring on dividends with the article and book, “How We Plan to Retire on Dividends (Amazon).” This article will guide you to the basics of the stock market, preferred shares, bonds, and the mindset of an investor. I highly recommend you take a look at this article or book.

How to Choose Your Stocks

Now, since you have read that article—,today, we need to focus on strategy. How exactly will we need to structure our portfolio to live worry-free lives overseas? There are many ways to extract our dividend income, so let’s look at the ones that best suit our needs.

The first step is to figure out precisely how much we need for expenses. To repeat, I said expenses—not all the money we would like to spend. For this article, we will use $2,000/month as our baseline expense amount.

I like to separate the expenses because I want to cover this money with closed-end funds. Closed-end funds are the closest thing to a paycheck that exists on the stock market. CEFs are actively managed and sacrifice capital gains for high yields. They give us immediate income.

I want my CEFs to pay for all of my living expenses—in this case, $2,000. CEFs have a high dividend yield, so it can be safe to assume we can achieve a 7% yield. With that 7% yield, we would need roughly $350,000 in our CEF portfolio.

I highly recommend you use separate accounts for all the different strategies I talk about today—no need to mix them all. Above, I have my high-yield portfolio, courtesy of Well Fargo Brokerage. I have some low-yielding index funds in this account, but the yield on cost is roughly 5.7%. Not too shabby.

52 Weeks of the Dividend Challenge

I would start most of these strategies early and at the same time. Your CEFs will be vital as you get closer to relocating overseas. However, the other methods will take years to get into a position to assist you, so start those today. Let’s take a look at the different investment strategies we can use on top of CEFs.

Dividend Growth Investing. We can use CEFs as the base of operations for our overseas lifestyle. We don’t expect capital gains from CEFs, just cold hard cash. Dividend Growth Investing will give us growth and income. DGI works best with time, compounding, and blue-chip stocks.

Having an extensive DGI portfolio layered on top of our CEFs will give us income and growth to ensure we never run out of cash for emergencies or celebrations. We can choose to reinvest the dividends each month or have certain stocks pay us in cash. With dividends, you are the boss.

$1,000 Dividend Shopping Spree

For my DGI portfolio, I use Charles Schwab. I have blue chips such as Altria (MO), Phillip Morris (PM), Public Storage (PSA), Costco (COST), Apple (APPL), and McDonald’s (MCD). The idea is to buy, dollar-cost-average, and reinvest until you are rich. If you don’t want to pick individual stocks, you may want to choose a dividend growth ETF.

Bonds. It is never a bad idea to have some bonds laying around. Having some long-term bond funds and high-yield bond funds in a small portfolio can help you build income and hedge against a market downturn. You can use bonds as a cash substitute.

I hold two bond funds in a small portfolio on M1 Finance. M1 Finance is excellent because you can have up to five different pies to separate your portfolios. I have my favorite bond funds, Vanguard Long-Term Bond ETF (BLV), and SPDR High-Yield Bond Fund (JNK) in my portfolio. I get a small number of capital gains and roughly a 4% yield. Not bad at all.

The Magic of Dividends

Index Funds. Index funds will not provide us any meaningful income, but they will keep our money flowing in the direction of the market. We may plan to be overseas for 20-30 years, so we will need to have our funds increasing with inflation. CEFs keep the lights on and the food warm. Index funds work in the background to grow our wealth in conjunction with the stock market.

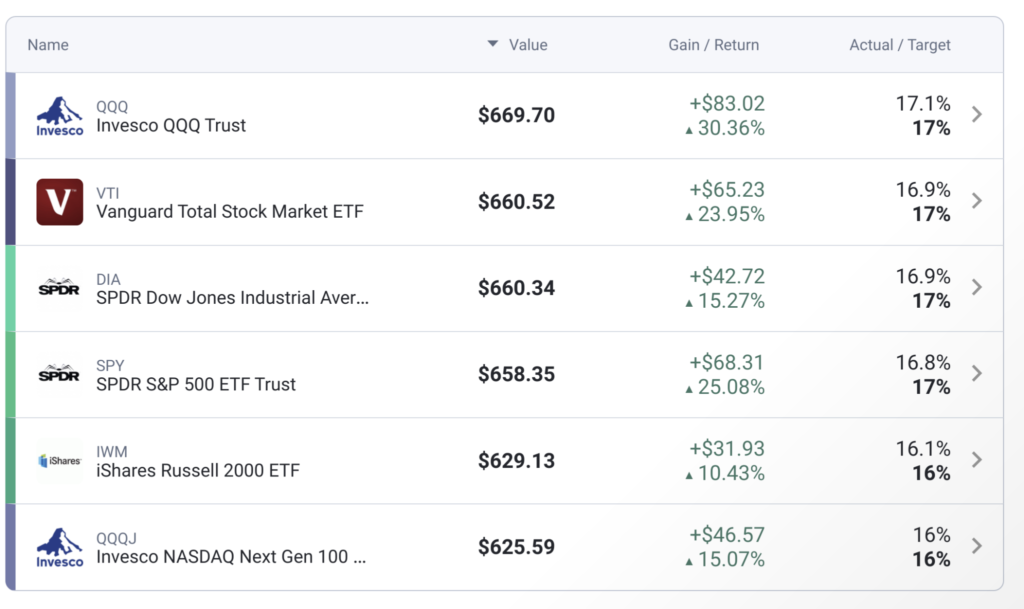

My favorite index fund is the Vanguard Total Stock Market (VTI). This fund covers us across the entire stock market. Just putting all your index fund money into this fund will diversify you across all the stocks on the stock market. M1 Finance is a great place to invest in index funds because it will auto-balance (and auto-sort) as you deposit a lump sum into your pie.

If you want to be a little more particular, you can invest in the different indexes. These include the S&P 500 (SPY), Dow Jones Industrial Average (DIA), and the Nasdaq (QQQ). They all have their unique quirks, but all are solid investments. I invest in all of them, however, the lion’s share of my index investing takes place with VTI.

Real Estate Investment Trusts. REITs are probably a better option than keeping a ton of rental properties in the States. Again, REITs work best with time and compounding. I wrote an article about REITs versus Rentals that will have a significant impact on your overseas lifestyle.

Why Do I Need to Invest in the Stock Market?

There are many sectors of REITs, and knowing which one can help you through your journey. For example, Mortgage REITs have high dividend payments but will cut their dividends as soon as interest rate trouble emerges. This information is good to know if you plan to live on their income.

That is one of the reasons I want CEFs to cover all of my expenses. Other companies can cut their income at a moment’s notice. CEFs can cut as well, but you are paying to have the top managers on your side.

Preferred Shares. Preferred Shares are great for income, but not for income that you depend on monthly. Companies can call their preferred shares at a moment’s notice, leaving you in the cold. You do not want to move overseas on preferred income and have a lot of your income called away. I have an article called “Preferred Shares vs. Closed-End Funds” that you might find interesting.

Selling Covered Calls. The great thing about having a DGI portfolio is that we can sell covered calls against the stocks in our portfolio. By selling covered calls, we are giving insurance to the buyer. However, if the price never reaches the strike price, we keep the premium and sell the call next month.

Dividends vs. Royalties part II

This income is in addition to our dividend income and capital appreciation. Selling calls is also a great way to stay up-to-date with our blue-chip stocks. Who says you can’t have your cake and eat it too?

Putting It All Together. As you can see, there are many ways to achieve success via dividends. Time and planning are vital to living overseas with dividend income. You do not want to try to accomplish this in five years.

I would say at least ten years to have a good enough base of income to move overseas. A 20-year horizon would be even better. Each strategy has its timelines to achieve your numbers. Each of these critical strategies reacts differently during major events.

Also, having a cash pile is essential to your overall well-being while living overseas. Bonds are outstanding, but they too can take a significant hit during a market downturn.

Dividends can be a great way to retire overseas, given the proper timeline and a large amount of invested money. Are they the best choice of all of our passive income sources? You will have to wait and see. Until next time, enjoy and happy investing.

- PDF of the Month: Don’t Gamble with Retirement 3+4 (696-Page Free PDF)

- Free PDF Downloads: Download FREE PDF books here

- Financial Mindset: Become CEO of Yourself (book)

- Retirement Planning: Don’t Gamble with Retirement 4 (Free PDF)

- Investing: The Pros and Cons of Dividend ETFs (Free PDF)

- Cryptocurrencies: The Magic of Cryptocurrencies (Free PDF)

- Real Estate: Real Estate is a Mindset (Intermediate) (Free PDF)

- Business: Retire Rich, Retire Comfortable with a Business 2 (Free PDF)

- Everything!: The Biggest Book on Passive Income Ever! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Sign up to Access our “Hidden” Free Kindle Book Schedule

- My first Children’s book: A Child’s First Book on Passive Income (book)

- Book Reviews: 54 Takeaways from 54 Books (book)

- Want to Build Passive Income from Books and Affiliate Marketing? (Learn here)

- Writing: Can Grammarly Make You a Better Writer? (direct)

- My Favorite Chromebook: The Ultimate Chromebook (direct)

- Follow us: On our Facebook Page and Join our Facebook Group

- Amazon Author Page: Check out my author page on Amazon

- Monthly Dividend Planner: Check it out on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply