Learning to invest can be intimidating, especially if you don’t have much guidance. That’s why I started the Investing for Interest 101 series (101, 102). Investing for interest (debt) can be safer than entering the stock market; however, you may achieve a lower return.

Previously we discussed the Super Safe Savers of high yield savings accounts, certificates of deposits (CDs), and Series “I” and “EE” bonds. Today, we will move into Treasuries issued by the US Government.

Safety in the USA. Investors consider treasuries some of the safest investments on Earth. When you buy a US Treasury, you put your full weight and confidence behind the United States of America.

What if Your House Paid Dividends?

Is there a chance that the US can default on your Treasury bond? Yes, but chances are if that happened, another country or aliens would overrun our country. You would have bigger issues than your bonds, as ammunition would be a higher priority.

Treasuries can fill an essential role in your overall portfolio, offer an excellent place to stash your emergency fund, and provide a fixed income.

I want to talk about where Treasuries can fit into your overall portfolio. First, let’s discuss the four types of Treasuries. There are many good articles on these instruments, so I will not reinvent the wheel. I’ll focus on how to leverage them.

The four types of Treasuries. The four types of Treasury debt are Treasury Bills, Treasury Notes, Treasury Bonds, and Treasury Inflation-Protected Securities (TIPS). Let’s explore these.

Treasury Bills. Treasury bills are short-term debt with maturities of 4, 8, 13, 26, and 52 weeks. Advanced investors use these to make quick profits. I never found the need to involve myself with these. Here is a great article on Investopedia.

Treasury Notes. Treasury notes are US debt that ranges between 2-10 years. Hardcore investors follow the 10-year note will great passion. I consider the 10-year note one of the most important things to learn as an investor. I will get into more about the 10-year note later. Here is an excellent article about Treasury Notes on Investopedia.

Relationships in the Metaverse

Treasury Bonds. Treasury Bonds range from 20-30 years. I personally spend all my time with the 30-year bond. I’ll go more into my use-cases below. They pay interest semi-annually so that you can use them for current income. Here is more detail on Treasury Bonds on Investopedia.

Treasury Inflation-Protected Securities. TIPS adjust their value depending on inflation. I don’t invest in TIPS directly; however, I invest in a TIPS bond fund. I will discuss more about bond funds throughout the series. Series “I” bonds also protect against inflation, and I find them easier to understand. Here is more on TIPS from Investopedia.

The importance of the 10-Year Treasury Note. If you consider becoming a bonafide investor (part 1, part 2, part 3, part 4, part 5), you must learn about the 10-Year Note. Investors follow the 10-year Note with great interest.

I may do a deep dive on the 10-year Note, but let’s talk briefly about it now. The 10-Year Note signifies investor confidence. When confidence in the economy is high, investors sell their 10-year Notes and buy other investment instruments like stocks.

The Magic of Passive Index Fund Investing

When confidence is low, or there is uncertainty, investors flock back to the 10-Year raising prices and lowering the yields.

Think of a 10-Year as a safety net. If Google (GOOG) stock is doing well, you are motivated to keep investing. However, if something shakes your confidence, you might take profits and move your money into the 10-year Note to wait for things to cool down.

This cycle plays out in the market almost every week, and sometimes we call it the fear/greed factor. Investors also link the 10-year Note to mortgage rates and other economic indicators. If you want to learn the ropes, start following the yield curve on the Treasury website.

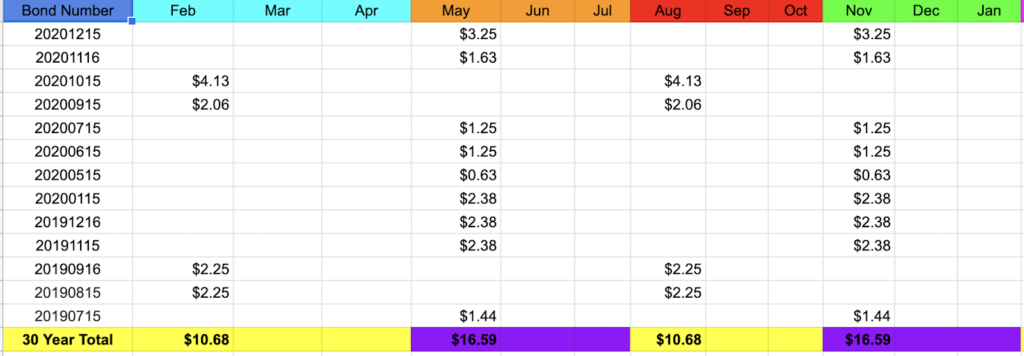

How I use my Treasury Bonds. I invest heavily in 30-year bonds. At least I did until the pandemic lowered interest rates to around 1%. The 30-year bond is a great place to build an emergency fund.

The 20 and 30-year bonds pay interest semiannually. They also have different schedules for payments, meaning that you can tailor your portfolio to deliver you four times a year.

For example, buying a bond in February will pay you in February and August. If you buy a bond in May, it will pay you in May and November. It is sort of confusing, but you will figure it out quickly. You buy your bonds on the Treasury Direct website.

Current income. I talk about Income Investing almost every day, and buying bonds is also income investing. You will just be receiving much lower yields. However, as we get older, we move into the asset protection phase of life.

Bonds allow us to get current income while having little to no risk. The government taxes interest at your standard tax rate, so you don’t receive tax benefits like dividends.

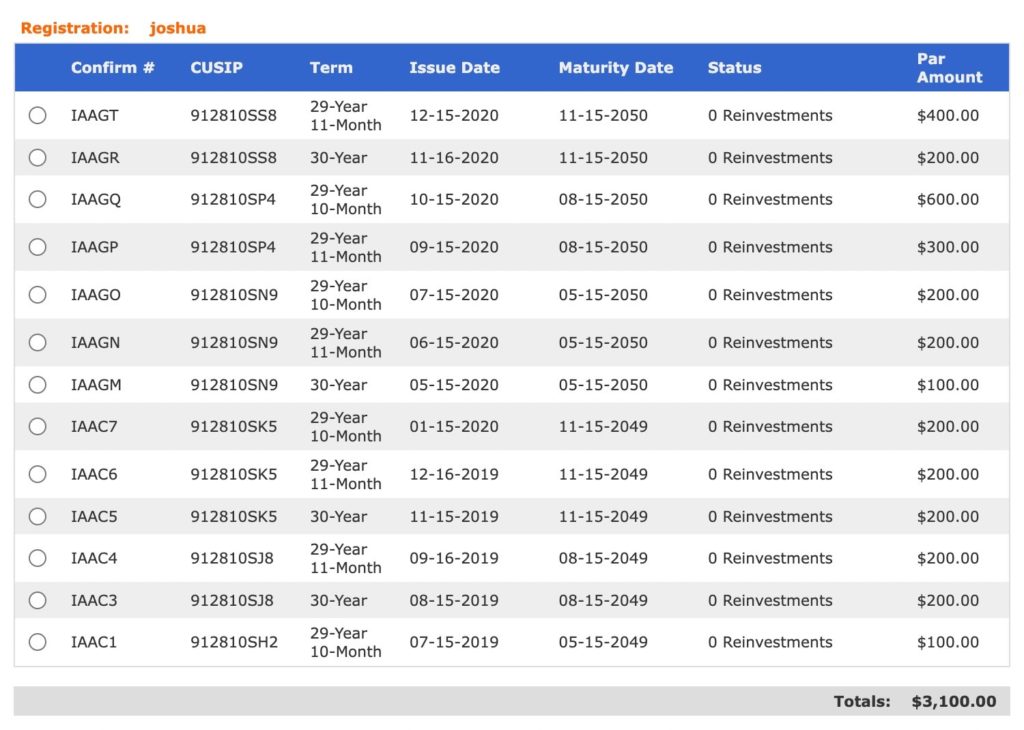

Luckily, I literally received my semi-annual bond payment today into my Wells Fargo Account. The good part of these bonds is that each one is its own entity.

You can set them up to pay you into various accounts. So, if you want to send your bond payments to an account with your wife or kids, you can custom tailor the amounts. It’s a nice perk vice investing in dividends where they tie you to your brokerage account.

The Magic of Dollar-Cost Averaging

Let’s get paid. Let’s take a look at the payments I received today. Again, I am an income investor, and I love receiving my money today. Keep in mind my combined interest rate is around 1.9%, so it’s not very high.

There you have it, nice and neat. I can now buy $10 worth of Peanut Butter M&M’s. Not a bad life at all.

Use cases. You can build an excellent income portfolio with safe instruments if you are just getting started. To create a safety net, you can use cash, high yield savings accounts, “I” bonds. Then uses 30-Year bonds for current income. Finally, layer on USDC for that huge monthly 9% yield.

That’s why I love investing. You can get a nice income stack without investing in the stock market. As we age, we can start using our dividend income to invest in bonds.

My Four Favorite Index Funds

Therefore you are converting your “risker” income into “safer” income. You get to keep your dividend stocks while adding income safely to your portfolio. With great knowledge comes great power.

If you plan on retiring overseas, it wouldn’t be a bad idea to have a large sum of Treasury bonds for income. They are safe, and you have many options to deposit the payment into various accounts. Sometimes being safe is its own form of return on investment.

Conclusion. I hope I have shed some light on the use cases for Treasury Bonds. Again, I don’t leverage the other Treasury debts, so I will only speak to what I use personally.

Yes, it will take a large sum of money to get a livable wage from Treasury Bonds. However, to get up to $1,000/mo is feasible over time. Once the rates get over 3%, I will be a buyer again. At that level, it is a fantastic return with nearly zero risk.

- PDF of the Month: Counting on Crypto 2 (Free 159-Page PDF)

- Free PDF Downloads: Download FREE PDF books here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 2 (165-Page Free PDF)

- Cryptocurrencies: The Magic of Cryptocurrencies (Free PDF)

- Real Estate: Financial Independence through Real Estate 2 (Free 123-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 2 (Free 185-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 5 (Free 431-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Crypto Exchange: My Favorite Crypto Exchange VOYAGER (Join Voyager)

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 54 Takeaways from 54 Books (book)

- Writing: Can Grammarly Make You a Better Writer?

- My Favorite Chromebook: The Ultimate Chromebook (direct)

- Follow us: On our Facebook Page and Join our Facebook Group

- Monthly Dividend Planner: Check it out on Etsy

- For more detailed analysis, join my Youtube: MFI YouTube Channel

New Year’s Passive Income Resolution 2022: Article (Amazon Book)

New Year’s Passive Income Resolution 2022: Blank-Lined Notebook (Amazon)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply