Buying a home can be an emotional roller coaster no matter how you try to fight your feelings. Some people worry about having a huge mortgage over their heads for 30 years. Others want to ensure they are buying the perfect home.

Today, we will try to remove as much emotion out of the home-buying process as possible. We want to think logically, rationally, and, most importantly, financially.

Buying your first home. Being a first-time homebuyer comes with many perks, so it’s best to understand and leverage them. I review many of the incentives you can use in the article “Maximum Leverage.”

Creative Financing in Real Estate 105: Hard Money

Everyone loves a first-time homebuyer—it may be because they are native or excited. But, we need to use this free attention to buy the best home possible—one that fits into our future vision of wealth and happiness.

What is a dream house? Let’s start by defining a dream house. A dream house is hard to define because it will always be a moving target. First, is it in your dream location? My wife and I love owning land, but we would be hard-pressed to find a five-acre plot in San Diego (where I am from).

What size home do you want? Your home size requirements can fluctuate depending on what size family you want to build. You may wish to have four bedrooms in a 2,500 square foot house. However, as we grow older, many want a smaller home because it’s easier to clean and maintain.

How much does it cost? The budget is usually the main concern for men, while the amenities for women. Keeping your cost under control can significantly affect your quality of life. The saying “house rich, cash poor” comes to mind. Please, don’t overspend on your home—your housing cost should be under twenty percent of your monthly income. Yes, 20%.

Creative Financing in Real Estate 103: Home Equity

What is an investment property? Usually, an investment property you buy to rent out immediately, not ever living in it. This distinction is important because the bank charges more interest for investment properties.

For the sake of this article, you will live in the home you are buying. You may live there for two years or ten, but you know eventually you will rent this home to tenants. You want that sweet, sweet rental income.

To buy a home with rental income as a priority, you need to buy a starter home—that means as small as possible. It is hard to find starter homes today because builders know most people want their first home to be enormous.

Starter homes are easier to rent, and you’ll have more profit margin when renting. It is easier to find a family to pay $1,500/month (when your mortgage is $1,000) than to find a family to pay $2,500/month (when your mortgage is $2,000).

Should You Buy a Property in a Small City?

Think about it, how many people will rent a dream house as they try to save for their own home? Chances are they want to rent a tiny home and save for their first house.

My opinion. Always buy a home as an investment property. Never let your emotions run rampant. That doesn’t mean you can’t have a beautiful home that your family loves. You just have to make the numbers work.

Our third home. My wife and I own three properties. House number three hit all the checkboxes as our dream home, but we also made the numbers work. The monthly mortgage was much higher than we wanted to pay.

However, since the home had two huge master suites, we knew we could rent them out to reduce our monthly expenses. We even got to the point where our renters covered our mortgage entirely.

This rental income means that we live in our dream house completely for free. It takes the right mindset to get lucky with money, so start building the mindset that can set you free.

Become a Bonafide Real Estate Investor: The 1% Rule

Because we can live in our home for free, that means our children can leverage that during their college years. They can have roommates that help pay the mortgage and generate cash flow. I wrote more about these situations in the series “Pay for College with Real Estate.”

A housing warning. On the other side of the coin, I see people paying tons of money for their first home. Even worse, they aren’t trying to build passive income streams to help reduce the costs.

If you don’t want to rent rooms, you can start a home business or become a content creator to help cover the mortgage. Trust me, your taxes and insurance will rise each year, and you will need to find a way to cover this gap.

I wrote an article titled “Your Income Should Increase Every Year” because inflation means your expenses will increase every year. I see young people paying 50-60% of their income towards housing costs. Do not be that person or those people!

Should You Manage Your Own Rental Properties?

What the future holds. You need to understand that your monthly savings rate determines your future wealth. If one couple saves 80% of their income, and another is saving 10%, which will become rich and retire happy?

The math is that simple. Don’t be fooled by Hollywood movies, where the lawyer making $200,000 has a huge house, a vacation home, two expensive vehicles, furniture, and takes luxury vacations. These are all lies!

These movies have given the average American hope to get rich just by working a job. You will never be rich just working a job and saving 10% of your income. And where do most people spend their income? On housing costs.

A quick example. It seems like everybody is making vast amounts of money, buying nice homes and cars, and living the American dream. However, only 10% of earners have a salary over $100,000/year.

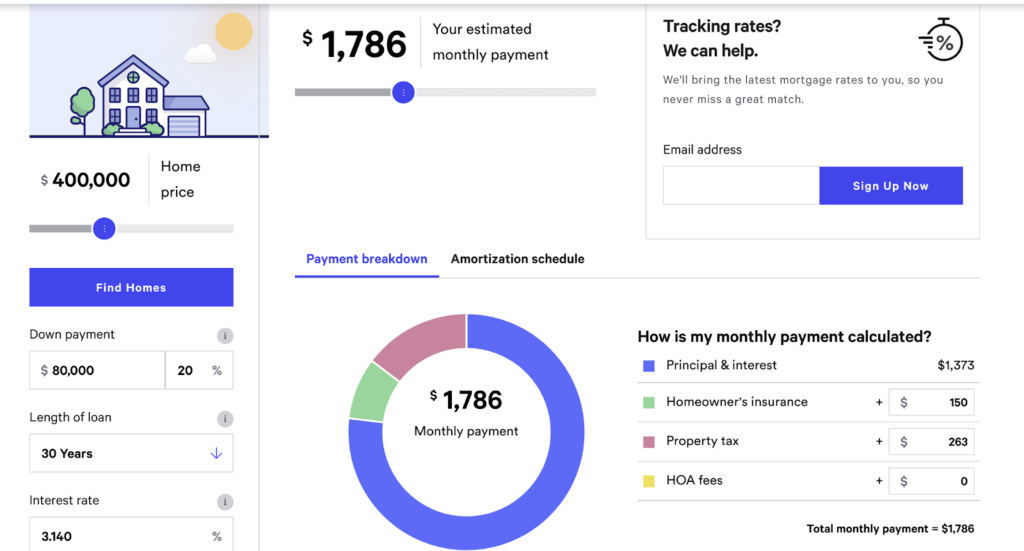

So when you see someone buying a $400,000 home, and they are making $100,000/year, do the quick math. They are making $7,000/month after taxes. With a 20% down payment ($80,000), their mortgage would be $1,800/month.

That means total monthly expenses with housing, cars, kids, and clothes would be roughly $4,000/month. What are the chances of saving $3,000/month towards retirement and investments?

RE Lifestyles 2: Investor vs. Lender

I would say that they would be saving roughly $1,000 towards retirement. That is not even saving towards a dividend portfolio and other passive sources. That gives them a saving rate of 14%. This puts them in the slow lane of wealth—waiting until they are 65 to achieve any kind of financial freedom.

Conclusion. Don’t be the couple above. Trust me, my wife and I made this mistake with our first house in 2008. It’s not a fun way to live, having to use credit cards to take vacations.

Whether you are planning to buy your dream house and live there forever or an investment property in waiting, crunch the numbers.

The article “Become a Real Estate Investor BEFORE Buying Your First Home” covers more about the mindset of buying your first home. I hate to watch young people sacrifice future happiness for the sake of real estate.

Your savings rate plays a huge part in your happiness. Knowing that you are building a dividend portfolio and investing 50% of your income will make you jump for joy. However, happiness isn’t free—it comes at the cost of living in reality.

- PDF of the Month: Become CEO of Yourself 2 (Free 196-Page PDF)

- Free PDF Downloads: Download FREE PDF books here

- Financial Mindset: Become CEO of Yourself (book)

- Retirement Planning: Don’t Gamble with Retirement 5 (Free 431-Page PDF)

- Investing: How We Plan to Retire on Dividends 2 (165-Page Free PDF)

- Cryptocurrencies: The Magic of Cryptocurrencies (Free PDF)

- Real Estate: Financial Independence through Real Estate 2 (Free 123-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 2 (Free 185-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Crypto Exchange: My Favorite Crypto Exchange VOYAGER (Join Voyager)

- Kindle Unlimited: I Why Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 54 Takeaways from 54 Books (book)

- Want to Build Passive Income from Books and Affiliate Marketing? (Learn here)

- Writing: Can Grammarly Make You a Better Writer? (direct)

- My Favorite Chromebook: The Ultimate Chromebook (direct)

- Follow us: On our Facebook Page and Join our Facebook Group

- Amazon Author Page: Check out my author page on Amazon

- Monthly Dividend Planner: Check it out on Etsy

New Year’s Passive Income Resolution 2022: Article (Amazon Book)

New Year’s Passive Income Resolution 2022: Blank-Lined Notebook (Amazon)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply