To become Bonafide investors we will need to comprehend the bigger picture when it comes to our investments. In Part I of our series, we talked about the difference between an investing insider vs. an outsider.

Today, we will discuss one of the most significant factors in your investment thesis: inflation. Inflation usually happens when the money supply has increased to the point where too many dollars are chasing after too few assets.

Consider today’s housing market. A house goes on sale, and within hours bids are starting above the asking price. The house will sell for above asking price. Now, the next place can base its asking price on the comparable home that just sold. Prices all go up—this is inflation.

Stocks vs. Cryptos

When it comes to judging inflation, we need to take a holistic approach. It is in the government’s best interest to state that inflation is under control. In fact, part of the Federal Reserve’s mission statement is to manage inflation.

The Bureau of Labor Statistics reports the Consumer Price Index (CPI) every month. Here is a must-read article concerning CPI on Investopedia. CPI uses a basket of foods, services, transportations, and medical care to gauge the rate of inflation. CPI controls the cost of living allowances for such things as social security, treasury bonds, and military pay.

Now, this is where we, as investors, have to dig deeper than the average person. We know that the prices of goods and services are sky-rocketing in today’s market. I can feel the effects when I go to the commissary. But where are prices really rising? In risk assets.

Risk assets can be considered assets that contain some form of price risk. The term risk assets can allude to real estate, stocks, bonds, gold, silver, and cryptocurrencies. They are sometimes referred to as risk assets because their performance can fluctuate depending on inflation, among other things.

CPI does not take into account the prices of risk assets. This means that the government may say that inflation is rising at 2%, but real estate has increased 10%, the stock market is over 15%, and cryptocurrency is 40%. These are all make-believe numbers, but you understand where I am going with this.

Dividends vs. Royalties part II

When the government prints money, the prices of CPI goods, services, and education do rise—however, the prices of risk assets sky-rocket. There are too many dollars chasing too few assets.

As a bonafide investor, we need to understand why the Federal government wants inflation to occur. They want to control it, but make no mistake about it; the government needs inflation.

Our government owes a lot of money to ourselves. We are creating treasury bonds that we, in turn, buy ourselves—this is how we print money in today’s government. We still have to pay the interest in these bonds, however.

5 Benefits of Options-Trading

The federal government attempts to control inflation, among other things, with the federal funds rate. The federal funds rate is the basis for such things as the treasury bonds rates, mortgage, and your savings account. The interest rates on your savings account are a derivative of the federal funds rates.

When the federal reserve lowers the funds rate to zero, it is trying to stimulate the economy. Usually, this means the fed is attempting to fight off a recession or depression. Let’s take a look at a few affected areas when the funds rate goes to zero.

Mortgage rates hit rock bottom as fed rates lower. Mortgage rates spur the economy by people buying and selling houses. However, prices and interest rates have an inverse effect on each other. The easiest way to understand the relationship between prices and interest rates is to look at a house’s monthly payment.

Let’s pretend that a house is worth $2,000/month. We can arrive at this monthly payment with a relationship of the price and interest rate. When the interest rate is low, the price goes up. When the interest rate is high, the price goes down. Right now, interest rates are rock bottom, so prices are sky-high. Understanding this relationship is key to forming our investing thesis in many areas, including stocks, real estate, and business.

Do I Need A Lot of Money to Start Investing?

New businesses began to form during a low-interest rate economy because there is “cheap money” everywhere. Banks want to originate as many loans as possible for the fees. Banks actually perform much better in a high-interest rate society, but more on that later.

For the most significant reason, interest rates affect our investments; low-interest rates force the average person into risk assets. I opened a high yield savings account at Discover bank in June 2019 with an interest rate of 2.2%. I was thrilled with this interest rate.

Today, my high yield savings account has an interest rate of 0.4%. I am not so happy now because this interest rate sucks. I keep roughly $5,000 in this account. My last monthly interest payment was $1.75. I can invest that same $5,000 into Pimco High Credit Fund (PCI) and get roughly $50/month in dividends. If I needed the money, I would at least move a portion of my money into PCI, maybe a $2,500 split.

The federal government doesn’t want your money in a saving account; they want you to be spending it in the economy. That’s right; the government wants you to spend your money. My favorite author, Robert Kiyosaki, puts it best in “Unfair Advantage” when he says, “savers are losers.”

Mailbox Money: The Power of Rents, Royalties, and Dividends

If you are trying to save money, at 0.4%, you will lose. Not only that, interest from bonds and savings are taxed at the ordinary earned income rate. So, not only are you receiving peanuts for saving but you are being taxed at the highest rate possible on these peanuts. “Savers are losers.”

Now, back to why the government needs inflation. Remember, they are borrowing money by selling bonds to themselves. The government needs to pay interest on these bonds. The interest is based on the federal funds rate and CPI. So if they can keep these rates low, then their interest payments will remain low.

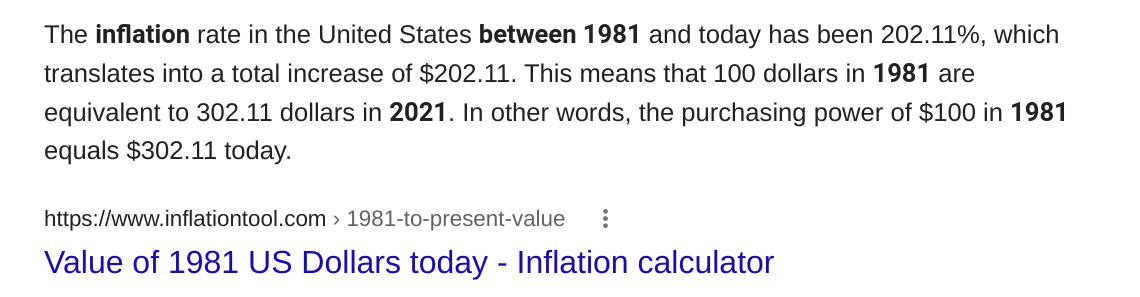

And if they can let inflation set to a certain extent, they will pay the money they borrow in cheaper dollars. Take a look at the value of a dollar from when I was born (1981) and today.

The fed needs inflation to set to a certain extent, but without it getting out of hand. If it gets out of hand, then they will have to raise the federal funds rate. Raising the funds rate will slow the economy down. The housing market will slow down, more people will become savers, and fewer businesses will start.

We can start to see this today. I like to track the 30-year Treasury bond as my clue of inflation. Most people prefer the 10-year treasury bond. When the fed lowers the funds rate in March/April 2020, the 30-year treasury interest rate dropped to an obscene 1.28%.

Now, the rate is creeping up to roughly 2.38%. Why is this important? Because at this yield, you are competing with some good dividend-paying stocks. Some of my favorites, such as McDonald’s and Johnson & Johnson, yield close to the amount of the 30-year treasury. I would hazard a guess that most people do not want to invest in risk assets; they would rather have a worry-free treasury bond.

Boring Investing is Good Investing

Now, what will happen when the 30-year treasury reaches +3% yields again? I would say a lot of money will leave the stock market. If it hits this amount, I would even buy $500-$1,000 worth of bonds every month. The stock market is great, but having a risk-free investment that can match inflation is just as lovely.

There is still a lot more to talk about with inflation coming. I will save that for the following article to cover how to prepare for investing before inflation. This piece was more of a background, but hopefully, you learned something. “Savers are losers,” the fed wants you to spend your money, and the federal funds rate controls your savings account are some key takeaways.

As a bonafide investor, you want to get to the point where you can form some of your own analysis. You can track your metrics and draw your conclusions. It may take some time to get comfortable looking at random statistics, but boy, does it become fun. That is the Become a Bonafide Investor Series’s purpose—to help you understand the bigger picture. Good Luck!

Read My Books for Free: Free Kindle Books Schedule also on Kindle Unlimited Join me on the best app for Crypto- Voyager

Follow us on our Facebook Page (here)

Join our Facebook group (here)

20 Books that Will Make You Rich (here) part 2 (here)

Follow our goal to Retire on CryptoCurrencies (here)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Leave a Reply