This year will be a challenging time for both savers and investors. The bond markets predict a recession, and the stock market is already pricing in the effects of inflation, high-interest rates, and limited commodities.

We can’t speak with certainty about what will happen in the next one or two years, so we must hedge our bets moving forward. The best time to invest your money is when markets are down; however, it is also the scariest time.

Welcome back to the Investing for Interest series (101, 102, 103, 104, 105, 106), where I discuss how to invest your money outside of the stock market.

Dividends vs. Royalties III

Today, I want to focus on savings bonds from the US Treasury, particularly Series “I” Bonds. I previously discussed “I” Bonds in the article “Super Safe Savers,” but now is the perfect time to strategize with these fantastic instruments.

A quick recap of “I” bonds. You can purchase Series “I” Bonds directly from the US Government on the TreasuryDirect website. Each individual or business entity can buy up to $10,000 of these bonds per year.

Series “I” bonds are unique because of the inflation adjustments you receive throughout your 30-year ownership. “I” Bonds have two interest rates that combine to give you the total rate of return.

The first interest rate is the fixed rate that the government imprints upon purchase. This number will always stay the same for the duration of your bond. From my 20+ years of experience owning these bonds, this first inflation number is never super high.

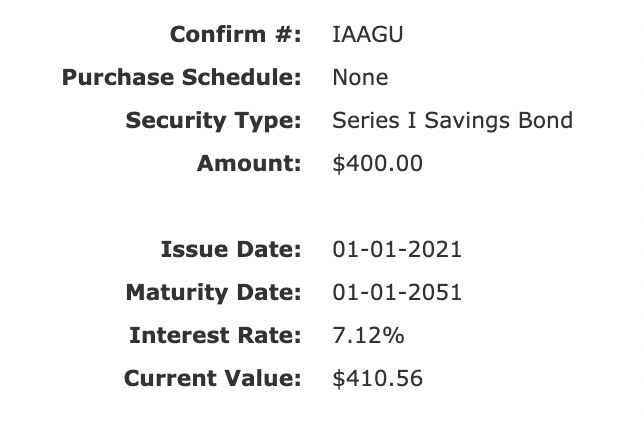

The government bases the second interest rate on the inflation index. Today, the rate is an impressive 7.12%. As you can see in the above picture, I have some bonds with a total interest rate of 7.33%. Thus, the first interest rate is 0.21%.

Fitness in the Metaverse

Why are “I” Bonds important to a healthy portfolio? I never thought of my “I” bonds as a worthwhile investment. When I joined the Marines in 1999, I signed up to buy a $25 bond every month.

Today, these “I” Bonds play a vital role in my portfolio. One of my eight steps to building a balanced portfolio is investing in “I” Bonds.

“I” Bonds can serve as part of your emergency fund because you can safely liquidate them during an emergency. So, you can benefit from the compounding of interest while you own your “I” Bonds, but keep them on hand for murphy’s law.

I wish “I” Bonds would pay interest directly to the owners during the ownership period, but that is the purpose of the 20 and 30-year Treasury bonds.

Budget vs. Fixed Income

Protection of capital. One of the essential functions of “I” Bonds is the protection of capital. As we age, protecting capital should be a top priority.

Of course, the safer we are with our money, the lower our returns. Because I am an income investor at heart, I like to have a portion of my wealth within safer investment vehicles—enter “I” Bonds.

Knowing that I have “I” bonds safely compounding in the background allows me to focus on my dividend growth portfolio and income investing.

Also, you don’t have to pay taxes on your interest until you redeem your “I” Bonds. If you know that you will have a slow financial year, redeeming some bonds may be a good idea. These redemption options allow you to capture your taxes as you wish.

Friendship in the Metaverse

The ultimate goal is investing. The ultimate goal of investing is to make the highest return in the safest manner. With inflation peaking, “I” Bonds will play an important part in your total returns.

There are not too many times in life that you can earn a safe 7.12%. The inflation interest rate adjusts every May and November, so following these rate changes is good. You can find it here. Apparently, the new rate will be over 9%, so stay tuned.

I admit that “I” Bonds fell off my radar for a few years. I like to see income coming into my account. However, these things are better than certificates of deposit and high-yield saving accounts.

Look at this Series “I” Bond I bought roughly 14 months ago. It has already received $10 of interest—unheard of in the fixed income world. That $10 will continue to compound for the next 29 years. We want to leverage compound interest at all times.

What Type of Home Should You Start 4: Content

Hedge against uncertainty. Finally, you want something stable with everything going on in the world. I like to hedge against the stock market, crypto market, and real estate market.

Any of these markets can go bust at any given time, and we have to reassess our portfolios. Good hedges are USDC stable coins and Saving “I” Bonds. I also like to publish books because I am earning income removed from the markets entirely.

Using all of these methods together, I can ensure I somewhat survive a downturn with my income intact. Yes, I will take a beating, but at least I will have a fighting chance. Plus, I may be in a position to buy into a down market—the best possible scenario.

Real Estate Investing in Your 20s

Conclusion. As you can see, Series “I” Bonds are part of a more extensive outlook for protecting your capital against adverse market conditions.

If you are a saver, these things are a must to protect your money from inflation. If you are an investor, “I” Bonds are a hedge against the various markets (real estate, crypto, stocks).

When you combine “I” Bonds with a small business or content creation, you also have financial protection if your job goes away.

We always need to hedge against something in life, and “I” Bonds are there to save the day. I admit I didn’t buy enough over the years because of low-interest rates (1-2%). But now that inflation has spiked, I see the true value of these bonds.

I am not the only one who learned from their mistakes, as I see many YouTubers singing the praises of “I” Bonds. I will double down this year and attempt to reach my $10,000 limit. How about you? Will you buy “I” Bonds this year?

- PDF of the Month: 505 Takeaways from 101 Books (pdf)

- Free PDF Downloads: Download FREE PDF books here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 2 (165-Page Free PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 2 (Free 123-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 2 (Free 185-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 6 (Free 409-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 2! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out on Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Crypto Exchange: My Favorite Crypto Exchange VOYAGER (Join Voyager)

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: Can Grammarly Make You a Better Writer?

- Best REIT- Fundrise: REITs vs. Homeownership (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Monthly Dividend Tracker (XLSX): Check it out on Etsy

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply