Being debt-free is one of the best feelings in the world, especially as a family of four. Any family person knows that running a household, especially in America, can be super expensive. It is a blessing to be able to manage our home on cash flow alone.

By the way, we have $800,000 of real estate debt. So, why don’t I consider this real estate debt as bad debt? Because some debt can be good for your overall ability to generate cash flow. Knowing the difference between good debt and bad debt is vital to our cash flow retirement. To go much deeper on this topic, please read “Rich Dad, Poor Dad.” Let’s explore.

Bad Debt. Bad debt is best described as consumer debt—buying things mainly because you want them. We buy most of the stuff with consumer debt, and they are liabilities. Liabilities take money from your pocket.

Happy Cash Flow Retirement

As we buy liabilities, we have to add them to our balance sheet. The balance sheet is a list of assets and liabilities. So our financed cars, boats, and RVs would all go on the balance sheet under liabilities.

Additionally, on our cash flow statement, the payment for our liability would be an expense. For example, our car payment would be -$500 in our expenses block.

It is crucial to make the distinction between the liabilities and the expenses. The importance of these separate blocks is that you want to know what you are collecting. If you are managing liabilities, you will see them building in your liability column.

Liabilities. Some liabilities are cars, boats, RVs, credit cards, mortgage loans, personal loans, furniture loans, student loans, etc. Take the time to write out your liabilities in the block. It may be staggering but indispensable. Trust me; I had my own heart to heart with debt. It wasn’t fun, but now that we conquered it; the feeling is beyond amazing. Please read my article “From -$77,000 to +$150,000 in 22 months.”

Expenses. Now that we have our liabilities written down let’s add the payments in the expense block. Some costs are car payments, boat payments, RV payments, credit card payments, mortgage payments, personal loan payments, furniture payments, student loan payments, etc.

Remember, there are still more expenses that will probably never go away, including gas, electricity, internet, cell phone, private school, etc. The goal of life is to keep the expenses block as low as possible. If you can do this, you can increase cash flow significantly.

Performing this exercise may make you realize how to close running a household is to running a business. These concepts do overlap but running a business is more complex. However, you can see the underlinings of business in your household. If you can run your house as a business, you can be very successful in trying to make a profit.

Are You Too Old to Start a Business?

The poor and middle class spend their days collecting liabilities and adding their payments in the expenses column. There is a better way.

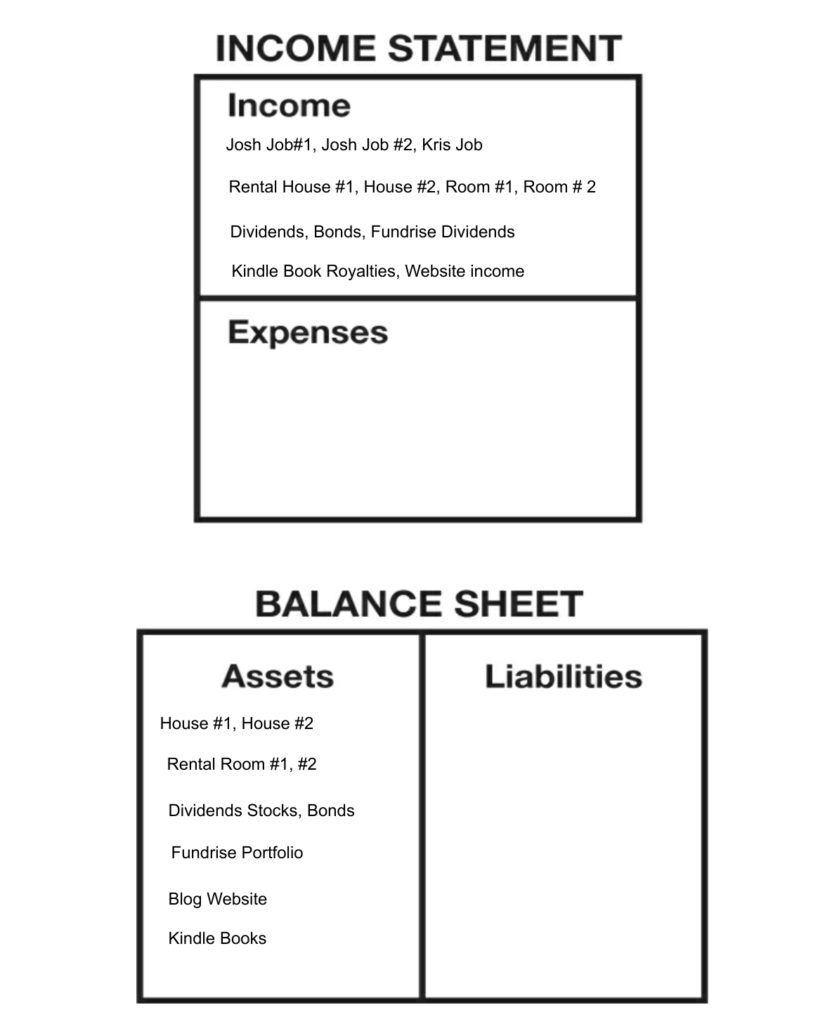

Assets. Assets are anything that puts money into your pocket. Assets can be businesses, real estate properties, books, videos, patents, investments, etc. Your job is not an asset. However, the income from your job can go in the income block.

Let’s take my assets column, for example. It consists of dividend-paying stocks, bonds, Fundrise REIT account, rental house #1, rental house #2, rental room #1, rental room #2, blog website, and Kindle books.

Mothers as Entrepreneurs

So I am spending my time collecting assets and putting them into the asset block. The rich spend their time looking for assets to fill up their asset column. Now let’s look at the income block.

Income. The income block is essential to your household because it is the start of the entire process. If you have a job, then employment income would begin in the block. Then you would add in all the revenue from your assets.

Is my personal residence an asset or liability? That is a question that you will have to ask yourself. Does it make you money or take money out of your pocket? My house is an asset because we rent out the two master suites. The money from these rooms has made us financially free.

Now we can return to the question of good debt vs. bad debt. If you are using debt to acquire something, you will have to ask yourself if it is an asset or liability. The item is neutral; it is the purpose the item serves that makes it an asset or liability.

$30,000/month Cash Flow Retirement

The simplest example is a car. If I buy for the sole purpose of going to work, is it an asset or liability? For me, it depends. How much do you make, and how much did you spend? Most people will need a car, but buying an expensive sports car just to go to work is a liability.

What if you bought a car to start a rental business? The business clears $100/month profit after expenses. Yes, it is an asset. It brings in money. You can do the same for boats, RVs, and other vehicles.

When you are looking to add debt or leverage to the balance sheet, ensure that the item is an asset. Your balance sheet will continue to grow by counting assets, and so will your income. Again, this is how the rich become rich, and more importantly, stay rich. I will have much more coverage on debt in the future. Understanding and using leverage (debt) is vital to your overall wealth-building processes.

Read My Books for Free: Free Kindle Books Schedule

Check out our Merchandise Shop on Redbubble: (here)

Follow us on our Facebook Page (here)

Join our Facebook group (here)

Follow us on Pinterest at:

https://www.pinterest.com/kingmarine/military-family-investing/Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Leave a Reply