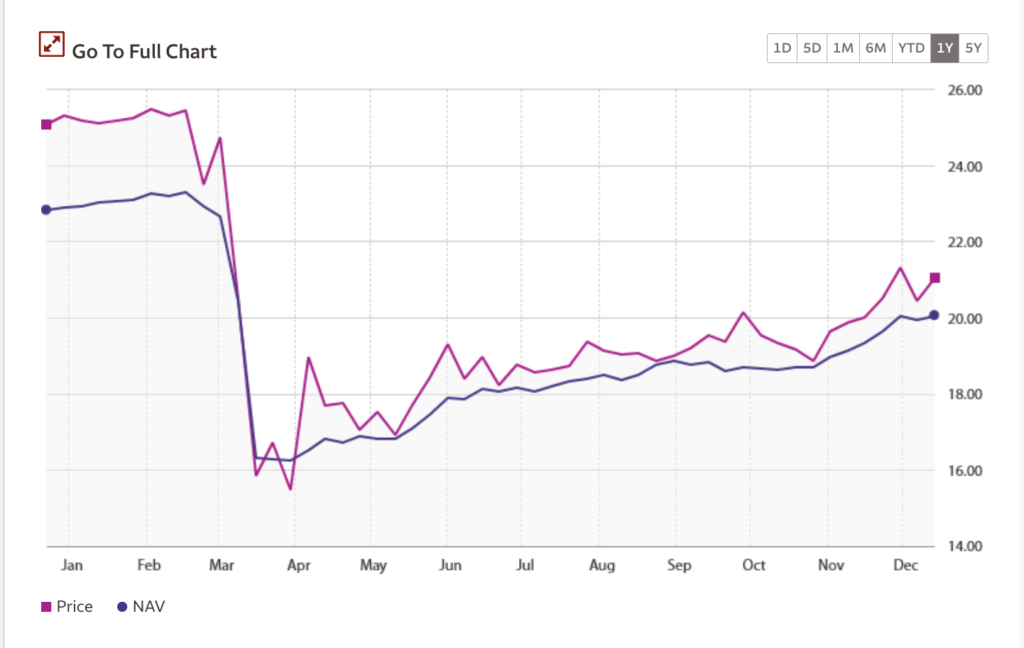

“How to Retire on Dividends” by Brett Owens and Tom Jacobs, is a hardcore take on how to retire on dividends. I say hardcore because you will have to study each and every one of your purchases to evaluate if you are purchasing at the right time. Don’t worry, they provide us with information on exactly how to do this. Common wisdom says that when we retire, we will use capital gains in order to give us income. But the strategy in the book will only use dividends to achieve this. Using dividends, we shot for an outstanding 8% dividend yield. An 8% dividend yield would produce $80,000 worth of income from a $1 million portfolio. How do we get to an 8% yield? By using closed-end funds of course. Closed-end funds are very similar to mutual funds and electronic traded funds, in that they are a basket of stocks or products. However, they have a fixed number of shares. Standard mutual funds and ETFs continue to add shares as more investor money pours in. This allows closed-end funds to have an important metric, Net Asset Value (NAV). By learning what each closed-end fund NAV is (you can find it easily), you can find out if it is trading at a discount or a premium. If it is trading at a discount to NAV, and it is a great fund, you can buy it and reap the rewards. I will post a picture of my favorite closed-end fund (PCI), and you can decipher if it is trading at NAV, above NAV, or below NAV. After you evaluate the picture, you will see 5 more takeaways from “How to Retire on Dividends”.

1) You do not want to sell your shares to fund your retirement. It is the reverse of dollar-cost averaging. This means that you will sell more shares when prices are low, and fewer shares when prices are high.

2) Most investors “buy and hope”. They pick up shares and root for them to appreciate in value. However, if you can study a good closed-end fund, you can see a hard metic in NAV. And based on the NAV, you can make solid buying decisions.

3) Closed-end funds are actively managed. This means the funds have a manager. You truly buy a closed-end fund based on the manager. You pick the “jockey” not the “horse”. Study the managers and you will make great buying decisions.

4) Mangers navigate the risky and tricky world of “sub-investment grade” products, so you don’t have to. Each product, i.e. a bond, has an investment rating. Once you get to the lower ratings, big investment firms and ETFs cannot, by law, invest in them. This leaves CEFs to buy and hold these products. You are paying the manager to navigate these products. Sub-investment grade products offer higher yields than investment grade products. “More risk more reward”.

5) Municipal bonds are bonds that certain cities and counties issue to fund projects. A lot of these are not taxed at the federal level. You can buy municipal bond CEFs and not be taxed at the federal level on dividends. This also means that if you live in a non-income tax state, like Florida, you will not be taxed at all. I was sure to purchase my first municipal fund CEF while reading this book.

Closed-end funds were not the only investments that were discussed in the book. It also discussed Real Estate Investment Trusts, bonds, stocks, and how to make covered calls. I had already invested in all of these products (save covered calls) and reading this book enlightened me further to their magic. However, you have to study the product and understand when to buy it. Trying to time the market is a fool’s game, so learning about NAV and how to buy products at a discount to NAV is the key. Learning how each product is taxed is also vital to building your retirement portfolio. Mainly, having a combination of high-quality stocks, bonds, CEFs, mutual funds, ETFs, and REITs is a sure-fire way to fund a healthy retirement. Buying all these products at a discount can ensure even better returns. I highly recommend this book if you are starting to build a dividend portfolio and even if you are just curious about investment products.

Follow us on our Facebook Page:

https://www.facebook.com/kingmarine1775

Join our Facebook group at:

https://www.facebook.com/groups/231490384820780

Listen and Learn on YouTube:

https://www.youtube.com/channel/UCfoq4ILMCmesrmO_HXE53Jg/

Follow us on Pinterest at:

https://www.pinterest.com/kingmarine/military-family-investing/Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Leave a Reply