When I mention that I invest in the stock market, most people I talk to will give me a horrible look of fear. They cannot believe that I would risk my hard-earned money gambling in the stock market. And yes, the stock market is terribly scary for the standard, hard-working American. This is because they have not conducted any research or time into understanding the overall scope of the stock market and where they fit into it all. Before you get serious about investing in the stock market, I recommend that you read “The Intelligent Investor” by Benjamin Graham. It is a tough read, but well worth it. Even if you do not understand most of what he is saying, his main point is that 90-97% of people should be investing in Index Funds. I will get into Index Funds in a few moments, however, let’s start with why most people should be invested in the stock market.

The first step to investing in the stock market is to set your overall goal. The two most common goals are “To have my money work for me” and “To help my money keep up with and beat inflation”. These are the perfect reasons. There are many ways to safely accomplish these goals. However, if your goal is “to become rich”, sadly you have come to the wrong article. Trying to get rich in the stock market is the fastest way to become poor. When money is your end goal, you will make risky decisions that will not only compromise your profits but also your principal. You will hear most people say “On average, the stock market returns 8-10% a year.” This statement is from a historical point of view when researching certain indexes. So let’s review some of the different indexes. There are 3 major indexes that most investors follow. The S&P 500 is a collection of 500 top companies. The Nasdaq is a collection of mostly high-flying technology stocks. And the oldest is the Dow Jones Industrial Average, which is 30 of the older, more mature companies that are still relevant today. Then there is the overall stock market, which encompasses all stocks trading on the market. Each index has multiple funds that track their movements. My favorite index funds for each index are: the overall stock market (VTI), S&P500 (SPY), Nasdaq (QQQ), and Dow Jones Industrial Average (DIA).

Index funds track their respective indexes. But what does that mean? This means that if the underlying index has a good day, then the index fund will have a very similar day as well. In the example below, for the closing of December 10, 2020, the Nasdaq finished up about 66 points or about +0.54%. Then, if you look at its index fund (QQQ) in my portfolio, it rose $1.21 for each one of my shares.

Now, if the stock market averages 8-10% a year, and I have my money in index funds, shouldn’t my index funds also average 8-10% a year? Yes, yes, and more yes. This is why Benjamin Graham said that most everyone should be invested in index funds. Most investment people and managers cannot beat the market for more than 2-3 years. They spend a lot of time and effort in trying to beat the market; however, it is very rare to actually do it consistently.

Now that you have your money invested in index funds and growing at 8-10%, what is the overall goal of this? In the capital appreciation method, the goal is to use your underlying assets to fund your retirement and lifestyle. This differs from the dividend growth method, however, we will get into that in Real Estate Investing 102. The capital appreciation method does not rely on dividends to fund your retirement and lifestyle. It is one of the harder concepts to understand, so I will put it into a scenario.

Let’s say that we start investing at age 30 with $1,000. We will invest $1,000 a month for 30 years and grow at 8% a year. Using our compound interest calculator (https://www.investor.gov/financial-tools-calculators/calculators/compound-interest-calculator) we see that we would have $1,369,461 at the end of our 30 years. Let’s assume we put our money in an index stock called KING (imaginary). When we started, our shares of KING were worth $20. After 30 years each share is now worth $300. When we need income, we would sell shares of KING. For example, if we need $3,000 for the month of December, we would sell 10 shares of KING. The capital appreciation method is also good for taxes. You would not pay taxes until you had to sell your shares. If you didn’t need any cash, you wouldn’t have to pay any taxes. For dividends, you have no control over the dividends payments you receive.

If you are selling your shares of KING to fund your lifestyle, wouldn’t you run out of money? Yes, you very well could if you are not careful. This is where the 4% rule comes into play. Basically, the 4% rule states that you can withdraw 4% of your portfolio annually and still have the principal amount continue to grow ahead of inflation. This may be a little confusing so let’s look at a scenario. If, after 30 years of investing, I had $1,000,000. If the stock market returns 8% this year, it would increase my portfolio by $80,000. Using the 4% rule, I could withdraw $40,000 a year. If all played out according to plan, I would finish the year with $1,040,000 in my account. With this, my principal amount would continue to grow as I live my lifestyle. For me, being always the worry bug, if I needed $40,000 to live off of, I would have closer to $2,000,000 invested, just to be safe.

Whew, in a nutshell, you should start investing at the youngest age that you can. You invest automatically into index funds every month. You put your investing on autopilot. If the stock market goes down, even better. By dollar-cost averaging, you would naturally buy more when the stock market is low, and less when the stock market goes up. This is almost a foolproof way of investing, as I will show you below. I recommend having some diversity between the total stock market (VTI), NASDAQ (QQQ), S&P500 (SPY), Dow Jones Industrial Average (DIA), and Russel 2000 (IWM). Is this enough diversity? First, we need to remember that stocks should only be a section of our total retirement/lifestyle package. We want to use our 401k and Roth IRA, Real Estate, and Businesses to round out our retirement portfolio. As far as the stock market and investment portfolios go, is this enough diversity? I have my balanced total investment portfolio to include checkings, high yield savings, bonds, stocks, and real estate. For bonds, I buy US Treasuries at www.treasurydirect.gov. You can also buy bonds on the stock market.

Bonds usually act inversely to stocks. This means that when stocks are very hot, bonds are usually icy. And vice versa. Having some bond ETFs (electronic traded funds) in with your stocks is a good way to balance your stock portfolio. The amount of bonds you have is entirely up to you. Some people say 60/40 stocks/bonds. Others say that bonds should match your age. So if I am 39, 39% of my portfolio will be in bonds and 61% would be in stocks. Whatever the case, it is good to have stocks and bonds. Bonds are a safer investment vehicle, however, you will not receive as much growth. However, when you see your entire investment portfolio go red, like in March 2020, it is good to see your bonds doing superbly. And, if you need to sell some stocks, you can sell your bond ETFs (Electronic Traded Funds).

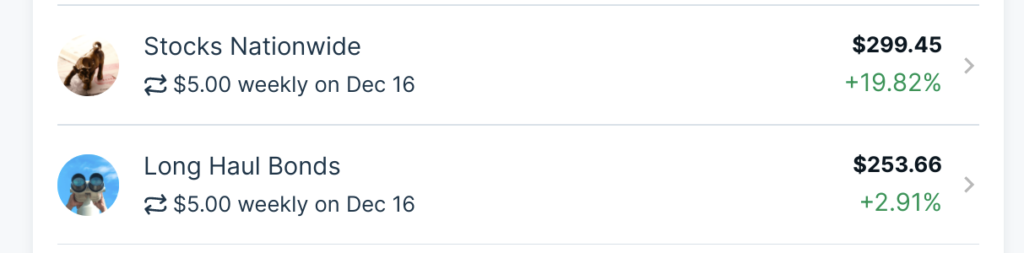

The bond funds I use are Vanguard Long term Bonds (BLV, 3.3%), High Yield Bonds (JNK, 5.07%), and iShares 20+ year Bonds (TLT, 1.62%). Look at the picture below. The top stock, Stock Nationwide, is VTI. And the bottom stock, Long Haul Bonds, is BLV. Right now stocks are on fire!! So VTI is far outpacing BLV. In fact, I have exactly $249 invested in both. However, if something crazy happened in the world (like a pandemic), people would try to sell their positions in VTI at a profit and put them into a safer investment in bonds. That is why bonds go up when stocks go down. So it is good to keep both on hand.

What would a good portfolio look like for the capital appreciation method? For me, and I am just one man, it would be 70% stocks and 30% bonds. Remember, I already have a solid government pension heading my way. If all my stocks disappeared, I would still be fine. You will have to evaluate your own situation. My personal allocation would be as follows:

—Index Funds——-

VTI- 30%

SPY- 10%

QQQ- 10%

DIA- 10%

IWM- 10%

——Bonds——

BLV- 20%

JNK- 10%

———————–

100%

To sum it all up, the capital appreciation method is the most hands-off method that there is. You set your investing platform to invest into your allotted funds and you let it ride. You would only have to check your portfolio once a month, just to ensure your funds didn’t close. I would re-invest all dividends as well. This would get you to your goal quicker. At retirement, you would have to sell up to 4% of your portfolio annually. However, if you had a pension, 401k, real estate, bonds, and/or businesses, you could let your money grow indefinitely and let your money continue to work for you. Stock Market Investing 102 will cover Dividend Growth Investing, which is almost completely different from the Capital Appreciation Method. Remember, this is the method that 95% of investors should be using. I recommend reading the book “The Intelligent Investor” (The Intelligent Investor – Benjamin Graham –https://amzn.to/3fKWvdu ). You can get started today with $1 into VTI and $1 into BLV on either STASH or CASH APP. Have fun on your journey to financial freedom.

Follow us on our Facebook Page:

https://www.facebook.com/kingmarine1775

Join our Facebook group at:

https://www.facebook.com/groups/231490384820780

Listen and Learn on YouTube:

https://www.youtube.com/channel/UCfoq4ILMCmesrmO_HXE53Jg/

Follow us on Pinterest at:

https://www.pinterest.com/kingmarine/military-family-investing/Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Leave a Reply