After about a year of investing and reading over 11 books in 3 months, I have finally come up with my solution to retirement. I have taken many things into consideration before presenting this idea to the general public, such as “Is it possible for most people?” “Is it achievable?” “Does it work?”. Those are things that we will have to discover on our journey. As of right now, I feel that this is a very achievable retirement plan, however, it takes education. It also takes more effort on the part of the retiree and I think that this will be the major hang-up with most people. In order to retire 4/50, you will need to be educated in business, finance, investing, budgeting, and real estate. By education, I mean self-education. Nothing in this retirement vision requires a college degree. I know this because I don’t have a college degree. First I want to go over what retirement 4/50 is.

Retirement 4/50 is a retirement vision that is based on cash flow. Cash flow is the difference between your income and expenses. If you have money left after your living expenses and bills, the rest of the money is considered cash flow. Most retirement plans are based on an amount of money that you would need to have invested in the stock market. With that money, you would live off 4% and pray that the remaining amount on money would still grow at a decent rate. In this method, you would be selling your shares in order to live off the income. Retirement 4/50 is based solely on cash flow. There is no total amount of money in the pot. You will try to reach a certain amount of cash flow.

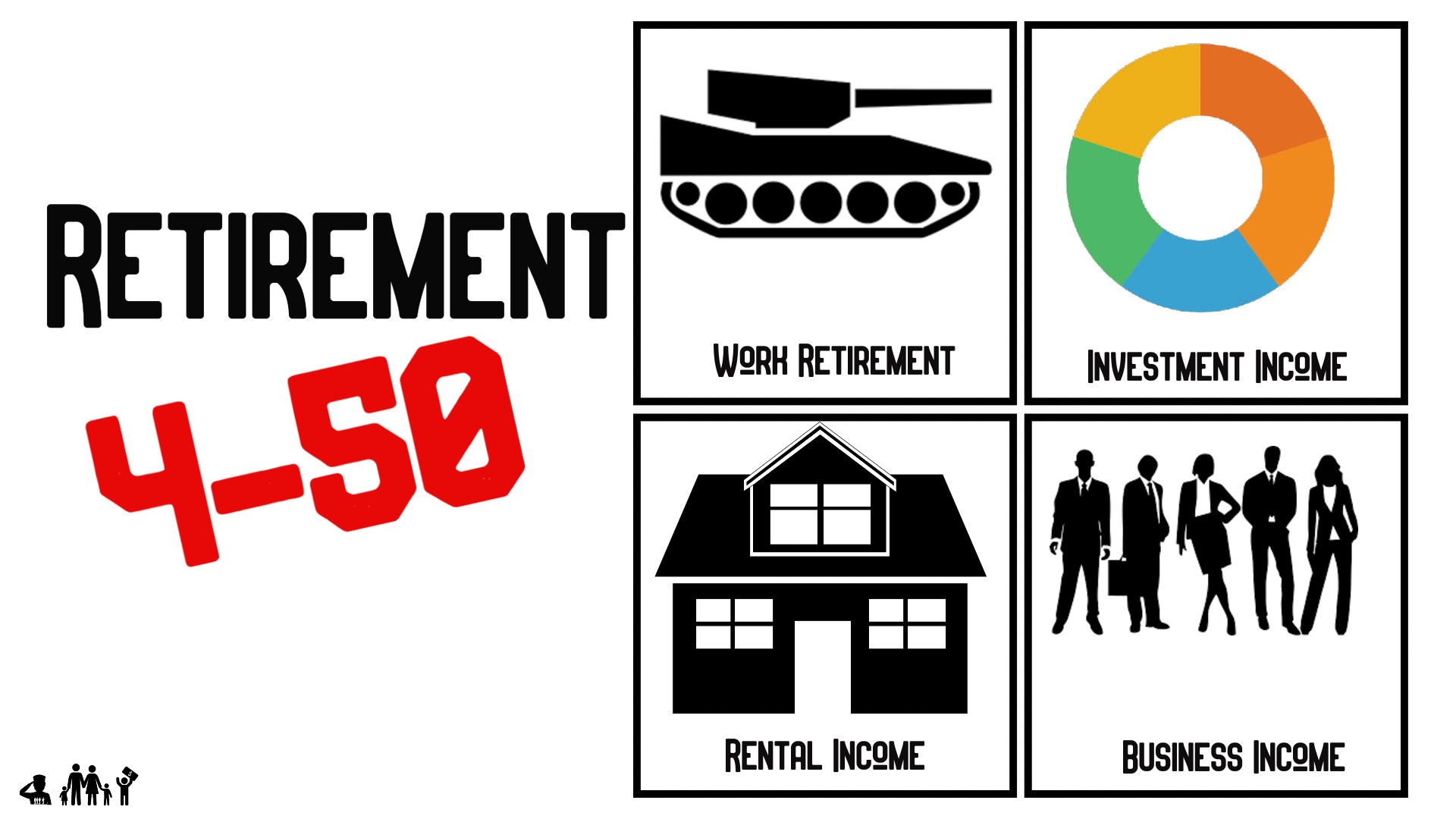

Why is it called Retirement 4/50? It is called this because there are 4 distinct retirement blocks that will be producing cash flow for you. The term 50 stands for the age at which you would become work optional. If you have done everything correctly, you will probably be financially independent by this point, but that’s not the goal. If you did everything it takes to become Retired 4/50, then chances are you are the type of person who will not fully retire anyways. Okay, so what are these 4 blocks? I am glad you asked.

These are my 4 retirement blocks! Now, let’s break down each of the blocks so you get a full understanding of the method to my madness.

Work Retirement- This is where most of us will start. We are employees in the workforce. Our goal from this block is to produce income EVEN when we are not working. How do you do that? Well, if you are in the military, you stay in until you reach 20 years. This will give you income. If you are not in the military, this is where your 401K will come into play. However, you will not be able to draw your 401K until age 59 ½. That is okay, if you are doing everything correctly, you will be work optional by age 50 anyways. You may need to lean on your other sources of income in that time period between or you can work a little longer. This retirement method has tons of options.

Investment Income– This is the combination of your High Yield Savings, Bonds, Stocks, and Real Estate (account). The Investment Circle is my personal way to create a balanced portfolio. I do not like having all my money in the stock market. So I keep around 40% of my portfolio in Bonds, Savings, Checking, and Real Estate account. All are outside of the stock market. This may lower my overall returns, but it bumps my overall safety. Again, each person can do all they please. My investing method is based on dividend investing and bond interest. With dividends, I will not have to sell my stocks in order to produce income. That is why I choose this method of investing.

Real Estate Income– This is the passive income that comes from rental properties or renting rooms. There are many ways to make real estate income. Some of the ways are rental single-family homes, rental multi-family homes, apartment buildings, commercial real estate, renting rooms, renting in-law buildings, and Airbnb, just to name a few. You can also buy storage facilities and I even saw that buying and renting billboards is an option. The chooses are unlimited, but at some point, you have to jump in. Most people buy a nice, big home and only they live there. This is a huge liability. This means it is taking money out of your pocket, every month.

Business Income- This is the part where everyone will go crazy. Most people do not want anything to do with business. However, a business can be very small. It can be a franchise, like McDonald’s or it can be a lawn-mowing service. You can also buy into someone else’s business. You do not necessarily need to be the person running the show. The key is to find something you love to do. Once you do that, plot on how you can help others with this particular skill. Once you figure out how to add value to someone else’s life, then you will be able to monetize your skill and assist others. The best thing about Retirement 4-50, is that you choose how much cash flow you want this block to produce. So if you say that you want $2,000 a month from your business block, then you can gear your business to be that big.

Those are the 4 retirement blocks. They are all vastly different but quite the same. They all require discipline and knowledge. In fact, in order to be truly 4-50, you will need to read and self educate, then you will need to find a mentor. Going into business and real estate may not be the easiest task out there. You need to prepare your mind for these journeys. Also, think about how much you would like to earn from each retirement block. For us, we want to achieve $6,000 per block, for a total of $24,000 a month. I think we can do this by age 55. Remember, we started late.

The best part of Retirement 4-50 is that you choose how much cash flow you want out of each of your blocks, and then you choose how you want to get there. For example, let’s say you wanted $2,000 a month from the Real Estate block. You could buy an apartment building with the bank’s money that produces you $2,000 a month. Or you could buy a single-family home and pay it off over 4-5 years. Once it is paid off, you would earn $2,000 a month in rental income. Now you have no leverage or debt on the property, it just took longer. You could buy a personal residence that had a large in-law suite. In the right market, you could charge $2,000 for it. Whatever the case, you have tons of options in each block.

I will go deeper into each block, our future plans for Retirement 4-50, and how to get started in future articles. Remember, you will not be able to achieve Retirement 4-50 without knowledge, education, and determination. Only 3% of society is built to have this kind of mindset. This is not for everyone. If it sounds interesting, please drop a comment below. Also, join our community. This is where like-minded folks can grow together.

Join our Facebook group at:

https://www.facebook.com/groups/231490384820780

Follow us on Pinterest at:

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Leave a Reply