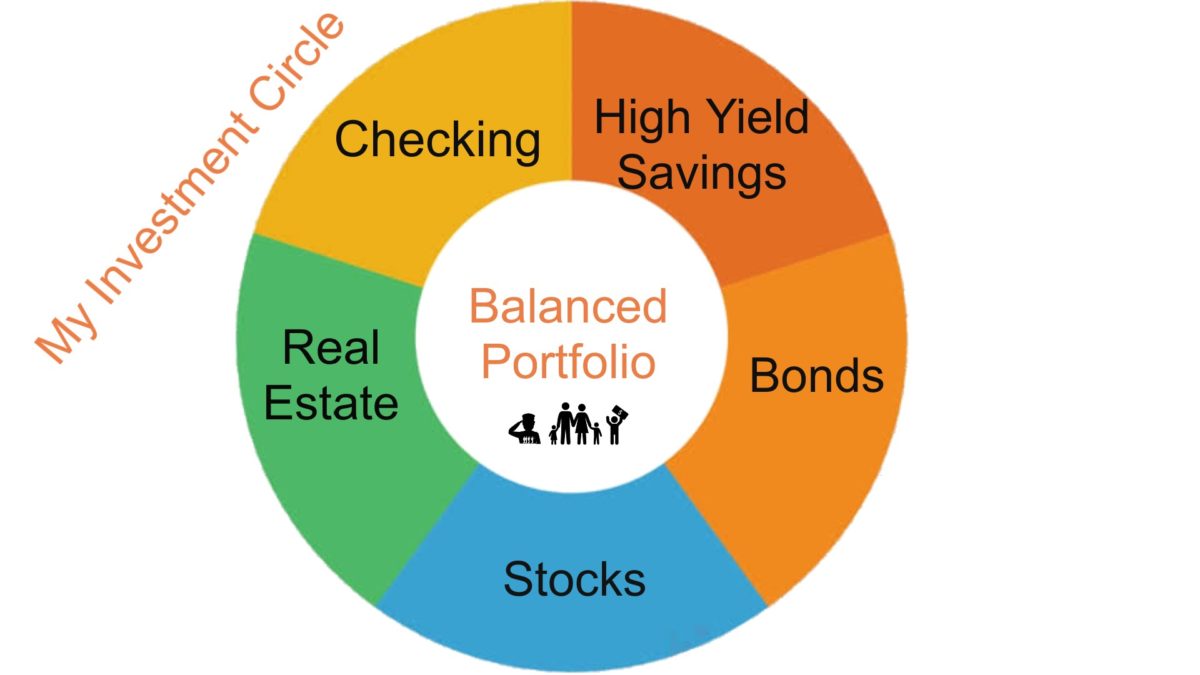

Creating your investment portfolio is an extremely personal affair. Only you know the amount of risk you can withstand. With that, I will show you how I choose to allocate my investments. Some may say that it is a little too conservative. That is okay. I grew up poor. I also don’t feel the need to have tons of money in the bank. I really want my family (parents, wife, kids, and grandkids) to be comfortable. That’s all I want. Let’s take a look at the 5 parts of my investment wheel.

1) Checking – You may ask why checking is part of my investment portfolio. To me, having a large checking account means you will not have to use credit cards ever again. I think of checking as an anti-credit card account. I never want to use credit cards again. Being able to have enough cash on-hand to cover day-to-day operations is a godsend.

2) High Yield Savings – A High Yield Savings Account (HYSA) is a good place to store your emergency fund. Your emergency fund should be about 6 months’ worth of expenses. I would start by getting $1000 in this account. Then slowly add to it. As long as your checking account can withstand most of the smaller emergencies, your savings will have ample time to grow. The HYSA I use is Discover Bank.

3) Bonds – I think of bonds as mini HYSAs. There are different bonds. I like the 30 years treasury bonds from treasurydirect.gov. These pay you interest every 6 months. So if I have a $1000 bond (@ 2%) it would pay me $10 every six months for 30 years. Then at the end of 30 years, it would give me back my $1000. It isn’t as much as some stocks, but it is safe, reliable, and accessible. If you get in a pinch, you can redeem your bond early with only a small interest penalty. So it is sort of like an emergency plan as well.

4) Stocks – Everyone loves stocks until everyone hates stocks. Stocks are super fun when they are going up, but not so much fun as they go down. But this is all part of the game as you invest in stocks. Never put any money you can’t lose in the stock market. Savings and Bonds are boring, but when the stock market goes down, you will never be happier that you invested in them. Having savings and bonds allows you to be a little riskier in the stock market. The stock market has something for everyone, but it will take a while (and a lot of reading) to discover how you want to invest.

5) Real Estate – I have my own physical real estate but I don’t consider this part of my portfolio. For mt portfolio, I invest in crowd-sourced real estate. The company I invest in is Fundrise. With the money you invest, they buy properties. I love Fundrise. They pay me dividends quarterly. The good part is that it does not fluctuate with the stock market.

So of all my investments, only my stocks go up and down with the…. stock market. Like I said earlier, the other investments are boring, but during a stock market downturn, there is nothing as exciting as your money staying static. This is my idea of a balanced portfolio. Yours could be completely different. That ultimately is up to you.

Join our Facebook group at:

https://www.facebook.com/groups/231490384820780

Follow us on Pinterest at:

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Leave a Reply