Over the last 15 months, my wife and I have been optimizing our lifestyle and finances to prepare for our future lives. We have cut down on household and entertainment expenses. We have begun to generate income outside of our standard jobs. And finally, we have began to invest in a balanced investment portfolio. Now, we need to truly take a look at what retirement looks like, financially. This blog post will serve as a sort of roadmap towards the way we are heading. We can swap different income streams around as long as it is replaced by another income stream. I find that it is important to have a goal to keep us on the road to a successful retirement. For us, a successful retirement means having the funds available to spend time (and money) with all of our family. We also want to be able to assist the family as they age and also as others began families. We envision our retirement to be bigger than life! That means that we need to start planning big, NOW!

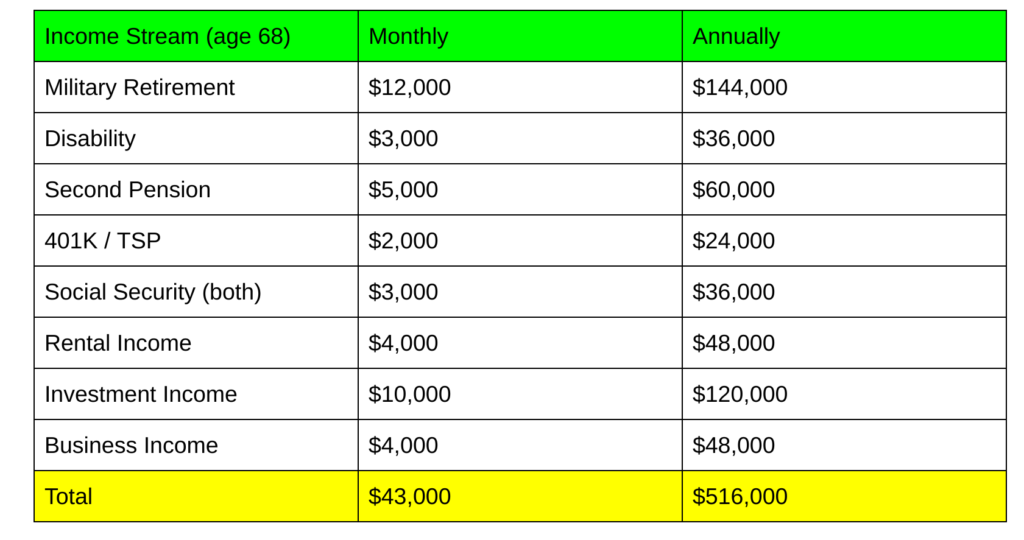

We will need multiple income streams to fund our future lifestyle. Not only will diversifying our retirement plan assist with making more money but it will also protect us as well. As much as we say pensions and investments are guaranteed, it is very prudent to diversify and plan for the worst. The income streams we are looking to tap into are; military retirement, disability, second job pension, 401K, social security, rental income, business income, and investment income. Below is an estimated overview of what I envision for us when I turn 68 (my wife 65). I have not done any research so far. After the table, I will go into a detailed breakdown of each of the different income streams. Finally, I will do another chart with my updated impressions. I am doing some of this research for the first time, so we can all learn together.

As you can see, I am dreaming HUGE! I went super big on investment income. If we are doing everything right, this should be very achievable. Now, let’s get into the detailed portion of the analysis.

Military Pension- As of right now, I plan on doing my 30 years in the Marine Corps, retiring at age 48. I will retire as an E9. Let’s look at what the retirement chart predicts for my retirement income at age 68.

It looks like military retirement will be close to an estimated $12,000 a month, before tax. Also look where TSP will be. It is around $4,000 a month. I don’t contribute a lot to TSP because the Marine Corps does not match my contributions and I can not easily transfer TSP wealth to my children. In my following government job, they will match, so I am more likely to contribute.

Disability- Disability is granted to service members that have suffered injuries (mental or physical) in the line of duty. No one knows what they will receive until they are evaluated during the final year of service. After 30 years of service, I honestly do not know what I will receive. However, I will plan for the highest. If I do not receive a 100% rating I will work to overcome this loss of income somewhere else.

Currently, a 100% rating nets you $3,279 a month, tax-free.

Second Pension- Right now, I am planning on working another 20-year job when I retire. Things could change at a moment’s notice. However, it is good to plan. And if I am working a 20-year career, it would be smart to work one with a pension plan. I predict I will work as a government service employee. Maybe as a GS-11 or GS-12. If I work as a contractor, I will compensate by putting even more money into my stock market retirement plan. Let’s take a look at the GS retirement plan.

The calculator was a little hard to use because it assumes you are serving in a GS capacity now. However, here is a rough estimate.

401K or TSP- I am not a huge fan of TSP, however with employer matching, it is very worth wild to invest in the program. I will assume that I leave the Marines with $30,000 in TSP. When I started as a GS employee I will start from that amount. Let’s assume I make $70,000 a year. I will contribute 5% a year and the government will contribute 5% a year. That will be $7,000 a year. I will use this amount for a 20-year career. However, in reality, my pay should see cost of living allowances annually. I will try to drain my TSP as fast as possible and convert it into other investment vehicles, like real estate or stocks. Remember, the only reason that I jumped into TSP was for the matching. I will withdraw at a 10% per year rate.

Social Security- Social Security is pretty straightforward. You can go to the website ssa.gov and see your projected amounts. Let’s take a look at my projection and assume my wife will make 50% of what I make. Social Security may not be a thing when I retire but I will assume it will be for now.

Rental Income- This should be interesting. We are going to assume that all 3 of our homes are paid off. The current rental market value for each home and room are as follows: Yuma house $1500, Pensacola house $1500, Pensacola room #1 $800, and Pensacola room #2 $800. For our predictions we need to look at historical rents over time.

Yikes. Prices went up at a rate of 3.06% a year. So let’s just double our amounts for now. That would be Yuma house $3000, Pensacola house $3000, Pensacola room #1 $1600, and Pensacola room #2 $1600.

Investment Income- I went pretty extreme on this one. But as you can see, if you are setting yourself up for success, you will be overly successful. There are two main types of stock market retirement strategies; growth and dividends. I prefer a dividend investment strategy. This means that I will invest in dividend-paying stocks. These stocks will pay me dividends that I will use as income. I will not sell my investments in order to generate income. Dividend investing is amazing but you also need a lot more to be able to generate sizable returns. I am shooting for a 3% dividend payout rate (yield). In order to receive $120,000 annually from dividends, I would divide that by .03. That means I would need $4,000,000 invested. This is a huge amount. I do not know if I can get there in 30 years, but I will try.

Business Income- Most people believe businesses are huge affairs with lots of employees and big office spaces. For us, we want to have a few side hustles that allow us to tailor our lives around our family. We would do everything from our properties. They could be things such as a small restaurant, wine, plants and fruits, bamboo farm, coaching, mentoring, motivational speaking, or blog. Any combination will do. We want to be mobile at this point in our lives. We may want to be in Turkey, Arizona, or Florida. Or we might be on a road trip. There are so many options on how to make money. The more successful you are, the more people will want to engage with you.

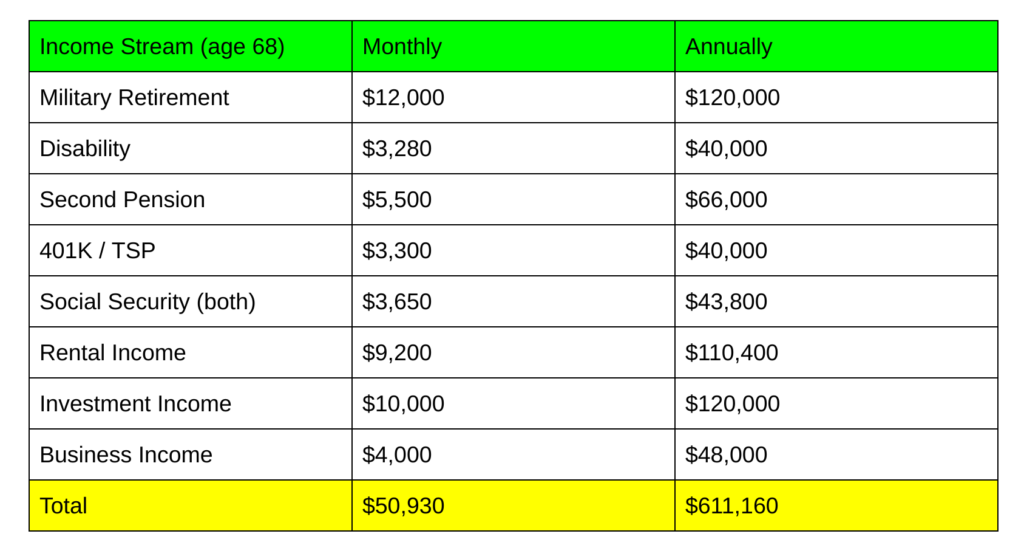

Whew, that was a lot of income. I learned a lot from doing the research. I honestly think that we will be doing even better than this. I know that my mom will leave me between one to two rental properties. There is a chance that a blog or seminar becomes a really big mainstream draw. So, there are ways to generate even more income. The trick is to invest it wisely. Let’s do the final totals.

WOW. I was even trying to be conservative. The main goals would be to keep working a job, side hustle, pay down homes, create small business with low overhead, and invest wisely. The rest will happen as a result of these accomplishments. What does your retirement plan look like?

Leave a Reply