The number one reason is that it is really fun. It is hard to believe that only 14 months ago (June 2019) I did not even have one brokerage account. It goes to show that once you jump into something, anything is possible. If you are reading this and don’t have a brokerage account, I highly recommend that you jump in. Once you get started, no matter how much you can stash away, it will snowball into success.

I have slowly opened my brokerage accounts over the course of this year. They all have the same objective; to generate income. I am all about producing dividends. Dividends are a share of a companies profits. A lot of dividend stocks do not grow in price at a very fast rate. When a stock grows in price, it is called price appreciation. For example, one of my favorite stocks is AT&T (T). Its price has ranged between $29-$40 for the last few years. However, T pays a 7% dividend. What I like to do is pair this stock with a stock that will appreciate more in value while paying a smaller dividend. For example, my Apple (AAPL) position has grown in value from $381 to $462. However, AAPL pays a 0.75% dividend. So when I add these two together, I get a decent dividend yield and decent price appreciation. That has kind of been my strategy across the board.

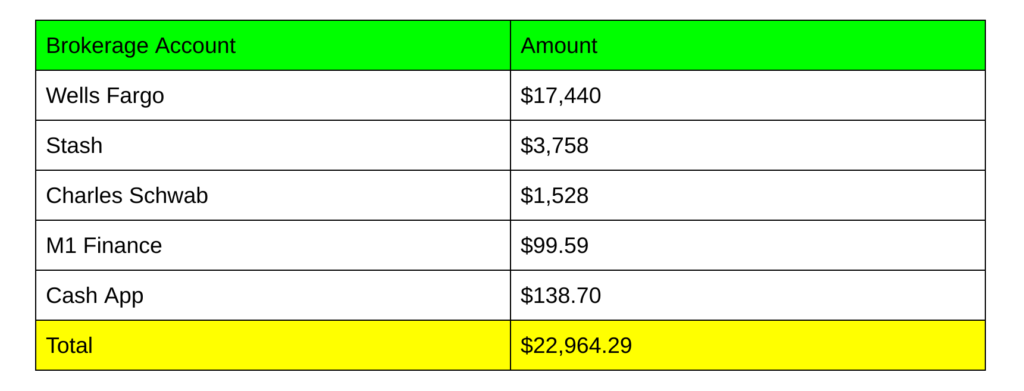

Remember, on top of all these brokerage accounts, I still have to be a well-rounded investor. A truly balanced portfolio has a high yield savings account, bonds, stocks, and real estate. I invest in all these categories monthly. The stock market is the most exhilarating of the bunch, however, it is also the riskiest. Ensure that you are also preparing your portfolio for the bad times by diversifying. Let’s take a look at an overview of all my brokerage accounts and then I will dive into each account platform individually.

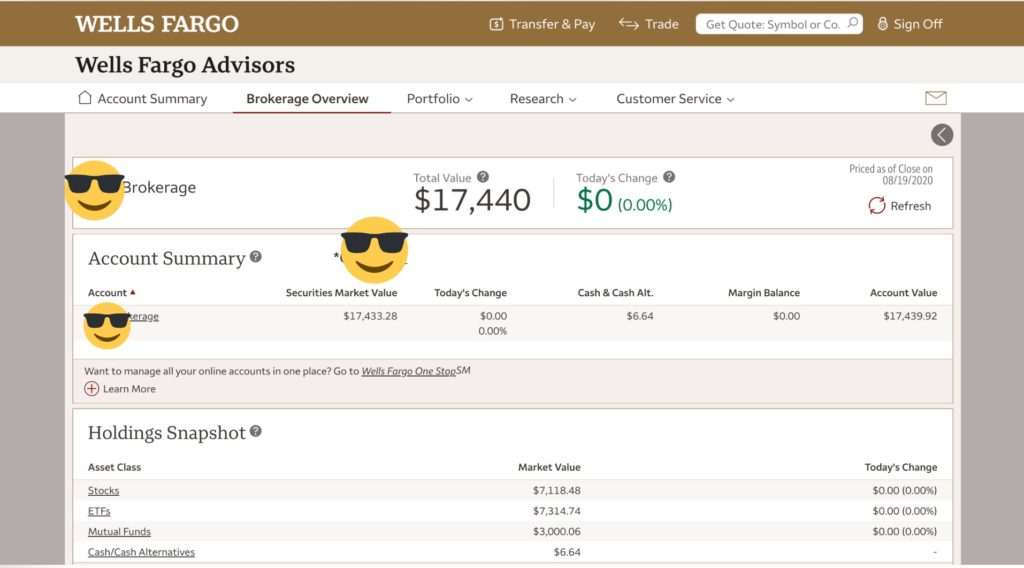

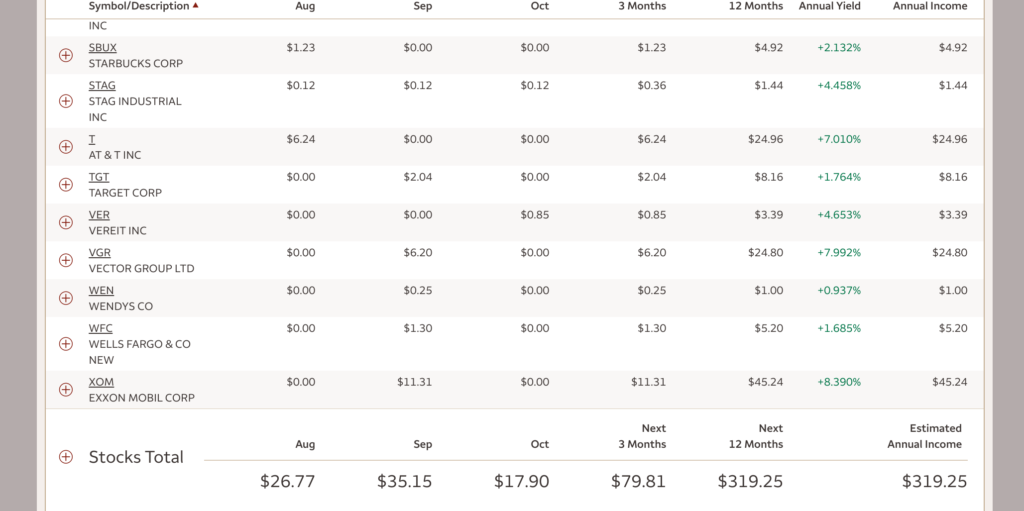

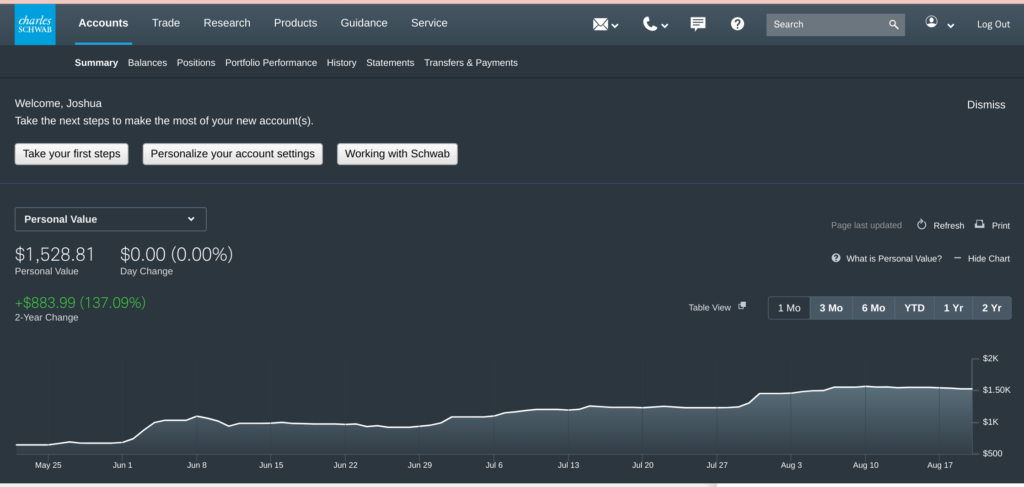

Wells Fargo– Wells Fargo is the granddaddy of them all. Wells Fargo is for advanced investors only. There is no handholding whatsoever. How I invest: Wells Fargo is my main account. I consider this as part of my investment portfolio. The others I consider side projects. Every month I invest heavily in Wells from any paychecks that I receive. It is a top priority to invest in this account because it is my main income generator. Pros: Wells Fargo has the most robust income tracker of all the platforms. You will be able to see every penny paid to you and also when it will be paid. Since most dividends are paid quarterly, it is easiest to track your different monthly payouts on Wells Fargo. Cons: They do not allow you to buy fractional shares. This means that you cannot put a small amount of cash towards a stock, you have to buy the whole thing outright. For example, if I want to buy a share of AAPL, I would have to pay the full $462. All the other platforms allow me to buy fractional shares, which is how I prefer to invest.

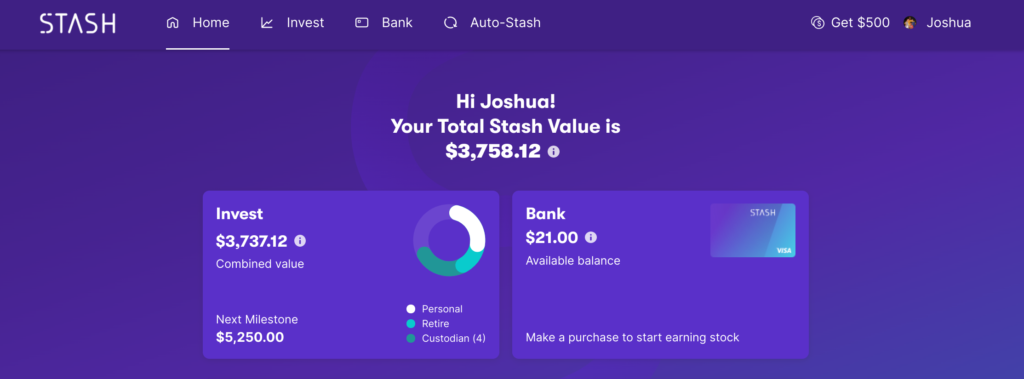

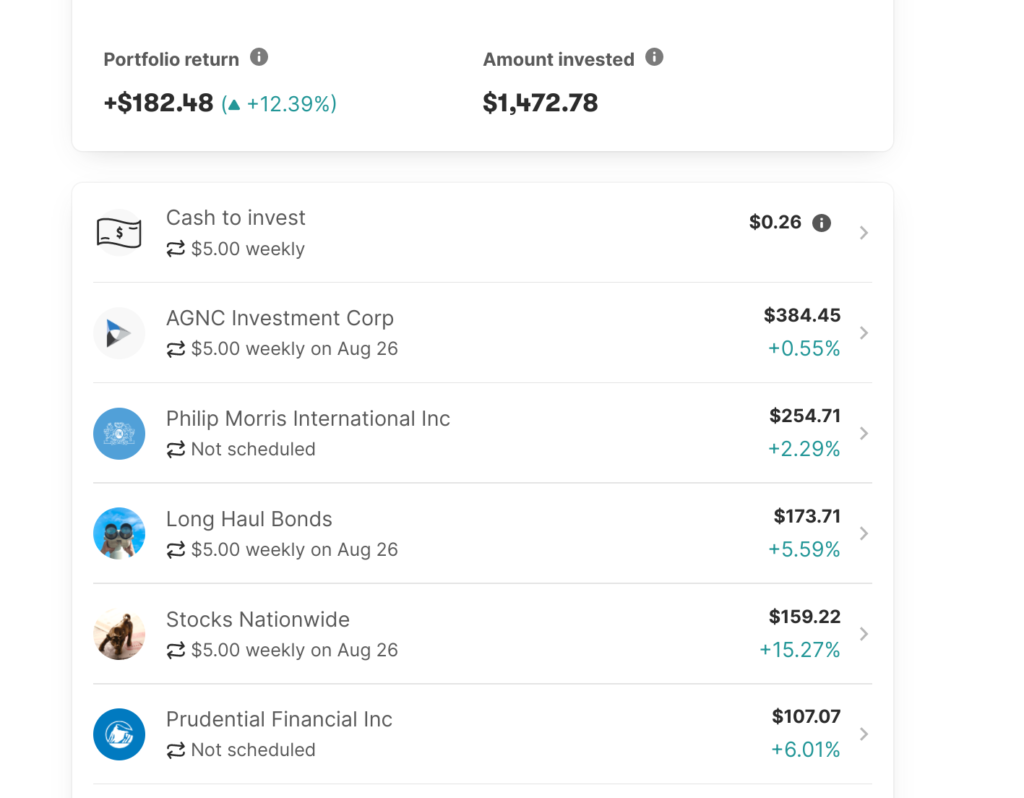

Stash– Stash is the easiest app to automate. If you like a hands-off approach, Stash is probably for you. I love the interface and every time I log in, I get happy inside. How I invest: Stash does most of the heavy lifting for me. I have it tied into my checking account. Every week about $110 is transferred into Stash and automatically invested. Easy. Pros: Stash has really good automation tools. You can drill down and invest in the companies you want, how you want. It is easy to put $5 on a stock weekly, for example. They also have things like smart stash and round-ups that allow you to invest even more money. It is super cool to log into Stash and have $9 to invest because they did a round-up from your checking account. Cons: It is very hard to track dividends and payout schedules. Stash is all about reinvesting into its portfolio, which is great. However, when I get older and would like to take dividends out, I want to know exactly what to expect to be paid.

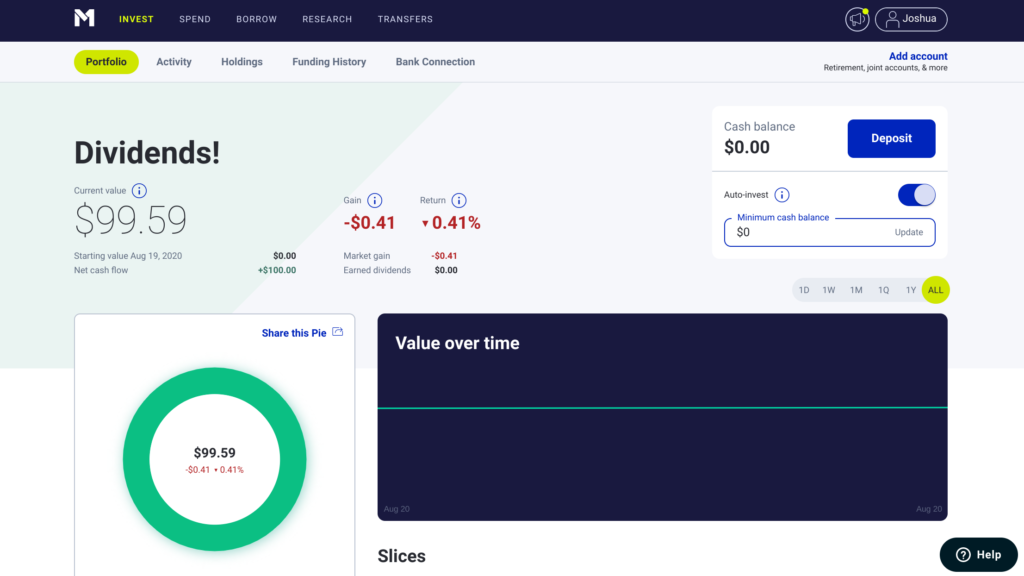

Charles Schwab– Charles Schwab is also for advanced investors. It has excess to all stocks and ETFs on the market. Stash, M1, and Cash app have a curated list of investment products. Sometimes you will not be able to find some products on these platforms. A good example is the gambling ETF, BETZ. It is fairly new (June 2020) and I have only been able to find it on Wells Fargo and Charles Schwab. How I invest: I use all the profits from my rental home to invest in Charles Schwab every month. Right now that amount is about $150 a month, but as rents go up, investments will also. Pros: Schwab is a full-featured brokerage. It has everything you can imagine. But it also holds your hand a little because you can buy fractional shares. This helps out with investing for me. I love having $20 and being able to buy into a few stocks. That is my preferred way of investing. Cons: Charles Schwab has good income reporting just not as good as Wells Fargo.

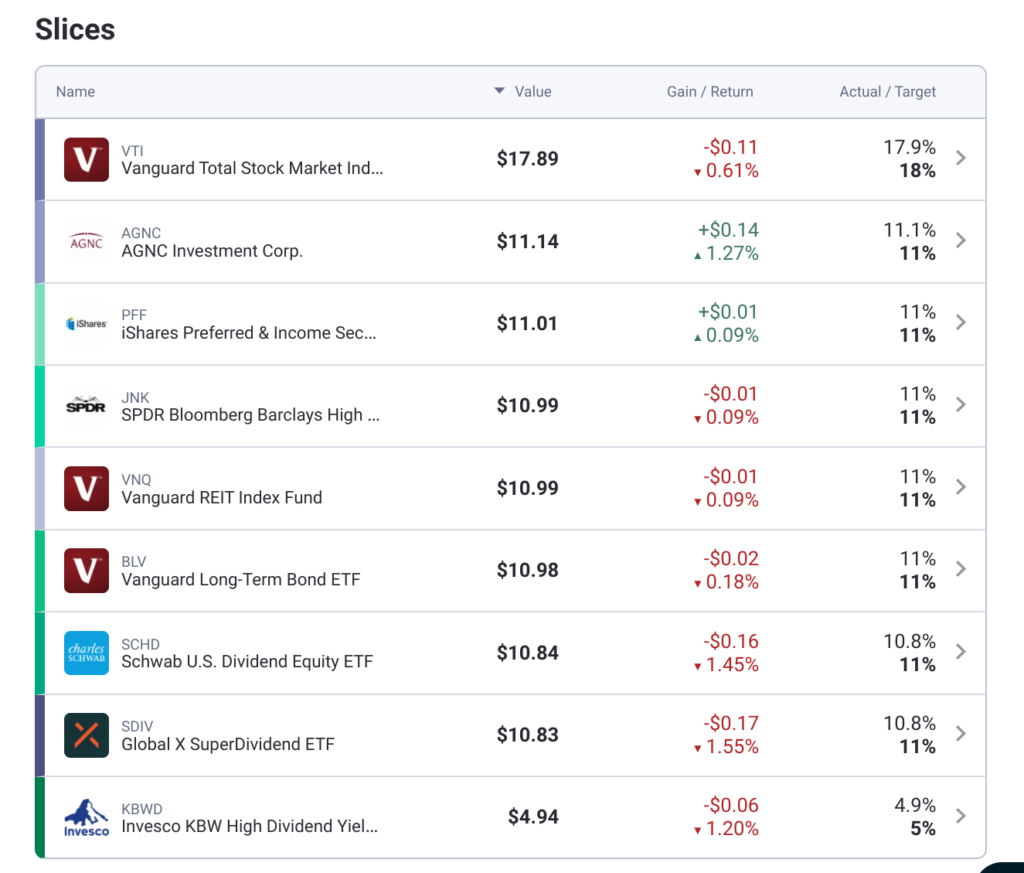

M1 Finance– I recently opened my M1 finance account (two days ago). I like the interface, however, it is a little hard to figure things out on your own. M1 basically will do everything for you. It will properly allot your money into baskets exactly how you tell it to. So when you add say $100 to M1, it will make all the necessary purchases in order to stay in your guidelines. It takes a little time to wrap your head around it but I really enjoy it. How I invest: My plan is to automatically transfer $100 a month into M1. I want to get a better handle on it. I plan on taking some side jobs here in Japan, so all that money will be invested in M1. Pros: The “pies” that you create are amazing. It is awesome to deposit $100 and have it decide how to best spend the money based on your preferences. I really enjoy this. Cons: The dividend calendar is not as robust as Wells Fargo.

Cash App– The simplest of the bunch. So simple that I was able to walk my Mom through the steps of investing over the phone. This is the app I recommend to anyone who is timid about getting into the market. How I invest: I use Cash App to control the spending of my personal budget. My budget is $60 a week, transferred into Cash App. When I have a good day of not spending, I invest money into Cash App. I love it because I have to tell myself that I don’t need this soda or candy. I can better use this money long term by investing. So it produces a great Ying and Yang type scenario. Pros: It drop-dead simple. It also is really fun to invest in the app. Cons: There is no income calendar or dividend payout chart. The information on each stock is limited. It really is for beginners.

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Leave a Reply